Understanding when the solar PV manufacturing ecosystem will recover from the sector’s second manufacturing downturn cycle is currently one of the most important questions for the industry.

This article presents a new analysis of the entire PV manufacturing ecosystem – including key materials suppliers – in which the financial health of all key stakeholders is considered; not simply a subset of companies in the value-chain looking to correct ailing balance sheets overnight, such as the leading polysilicon and module suppliers.

By comparing the best-in-class production margins for each segment of the PV manufacturing ecosystem to target percentages needed to operate in a healthy growth mode, the key phases of the current manufacturing downturn (onset, trough and end points) can be understood clearly.

The article concludes by considering what the PV manufacturing segment might look like once the current downturn is over and the leading participants are able to plan for the next 2-3 years (towards the end of the decade).

Chaotic entry to second PV manufacturing downturn

The second PV manufacturing downturn was inevitable once investments (capital expenditure, or capex) hit record levels in 2021. Only a bullish and somewhat elastic end-market demand environment prevented the downturn happening in 2022.

The delay in the manufacturing downturn cycle then created an artificial investment climate in China during 2022 and 2023, driving even higher equipment spending levels.

Therefore, when the downturn did start (at the end of 2023), the subsequent collapse in fortunes for PV manufacturers was more pronounced than seen during the previous (first) PV manufacturing downturn of 2012-2014.

New methodology to understand the entire manufacturing ecosystem

This article presents new research and analysis for the PV industry, where the success of the entire sector is shown to be dependent on each stage of the manufacturing value-chain, and the respective material suppliers, being profitable.

Essentially, this scenario is seen as key to getting the sector out of the current PV manufacturing segment downturn and avoiding a repeat of the period 2020-2023 when profits were skewed to specific segments of PV manufacturing, such as polysilicon and glass supply.

The analysis begins by examining the component-specific revenues and production costs (cost of goods sold, or COGS) for the market leaders (all Chinese companies) in the value-chain (polysilicon, wafer, cell and module) and materials supply-chain (focusing on the major contributions here – metallization paste, films/encapsulants, and glass).

Within each of these seven manufacturing segments, component-specific revenues/costs are backed out for three of the five market-leaders (by volume) in each segment, including the most recent third-quarter reporting (9M’25) by all these companies.

Note that, for many of the segments, the three companies chosen were indeed the top three by supply volume, making the validity of the analysis more pertinent and representative of state-of-the-art manufacturing today.

Within each of these seven segments (polysilicon, wafer, cell, module, paste, films and glass), the component-specific revenues and production costs for each of the three-entity groupings were consolidated prior to gross margin calculations (as opposed to simply averaging unweighted gross margins at the company level that would have yielded misleading output).

The findings alone here are interesting as a first step, but only when considering the seven segments in isolation, broadly confirming a sector that, since 2020, has seen various degrees of excess profits from discrete parts of the PV manufacturing ecosystem (in particular polysilicon during 2021 and 2022 and glass in 2020 to 2021), and excess losses (most notably from polysilicon, wafer and module producers through the downturn).

Not to forget the only part of the PV manufacturing segment that operates with a fiscal prudence and maturity not seen anywhere else – the metallization paste suppliers – where largely static gross margins are a consequence of the raw-materials-processing status in place for this materials supply segment.

However, the key goal of the research here is to understand (now that the sector is emerging from the downturn trough of the second PV manufacturing downturn) the extent to which gross margins still need to be restored in each segment; and by default, finally reaching a point where the downturn has come to an end.

The methodology applied within the analysis presented in this article is a simplified version of a technique called Analytical Target Cascading.

Use of Analytical Target Cascading to forecast the end of the PV manufacturing downturn

Analytical Target Cascading is a hierarchical system-level design tool used to optimize relevant contributing subsystems (or building blocks). For example, in a supply-chain where separate elements have autonomous decision-making agency for performance and profitability.

In the application here to the solar PV manufacturing ecosystem, the gross margins of the seven segments considered are each compared to specific target margin levels (so-called comfort zones of operation) and weighted by importance to the sector (or system) as a whole.

Therefore, in addition to simply backing out all the gross margins, this analysis requires industry knowledge for each of the segments in terms of target margin levels and relative sector importance. These partially-qualitative entries are done by looking at historic margins needed within each of the seven segments to sustain controlled investments (either by the addition of debt or through cash) and are by default China-related operating metrics given the dominance of China in PV manufacturing.

Correspondingly, the weighted sum of the subsystem (or segment) deviations (reported margins compared to target values) forms a powerful industry metric, representative of the overall manufacturing sector profitability (where ideally all segments operate profitably in their own comfort zones).

Therefore, if the output of this weighted summation is higher than the overall sector target, this implies excess profits being ‘kept’ at certain stages of the value-chain or materials supply-chain; consider the case-study of polysilicon margins during 2021 and 2022 for example being much higher than all other segments.

If the output is lower (and consistently declining), then the manufacturing sector is essentially in ‘recession’ – namely a manufacturing downturn phase.

However, the ultimate goal of the research is to understand specifically if the PV industry has reached – or passed through – its downturn trough, and when the downturn may come to an end. Not to mention, how this ‘ending’ may materialize and what the PV manufacturing sector will look like during the next upturn phase (overlapping with new capex and technology-spend commitments by the leading players).

When will the downturn end? What is a U-shaped downturn?

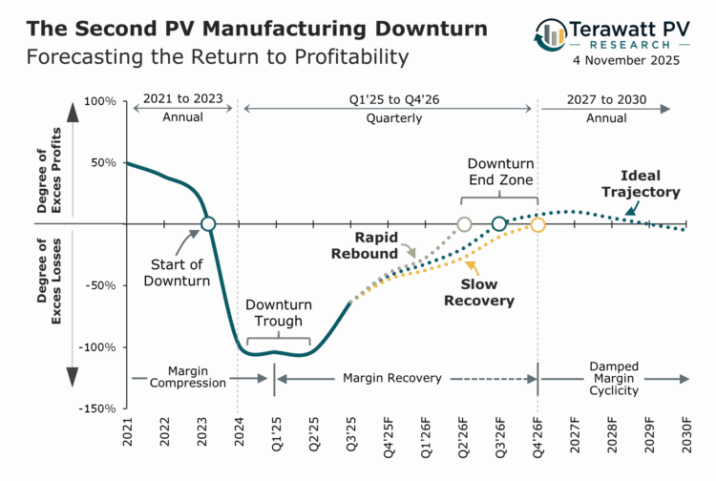

This section now discusses the major findings of the research, illustrated first by Figure 1, shown above.

The graph in Figure 1 shows the trajectory of the overall PV manufacturing profitability metric (the sum of segment-specific weighted gross-margin deviations from target values), over a period from 2021 to 2030.

The actual (observed/historic) values are shown by the solid blue line from 2021 to Q3’25. This then has three forecasted scenarios (the dotted lines) going from Q4’25 to 2030.

The period 2024-2025 is expanded (by quarters) to allow clearer focus on the downturn period and subsequent recovery.

The vertical (y-axis) scaling illustrates the level to which the overall PV manufacturing sector is either ‘over-performing’ from a margins/profits standpoint (degree of excess profitability as a percentage of the target), or ‘under-performing’ (degree of overall loss-making).

The starting point (2021) reveals a manufacturing sector operating well above target levels, mostly due to excess profits from the polysilicon and glass segments.

Seen at the time (during 2023 in particular), as polysilicon pricing came down rapidly (due to over-capacity/over-supply at the polysilicon stage), the entire manufacturing sector was ushered into overall loss-making territory that effectively became a prolonged downturn. One can consider the ‘Start of the Downturn’ as circa. Q4’23, shown on the graph.

This Margin Compression phase (that started as early as 2021 for part of the PV manufacturing sector) has continued through most of 2025 but crucially reached the low point (the greatest collective loss-making phase, or Downturn Trough) during a three-quarter period from Q4’24 to Q2’25.

While hitting all-time loss-making levels for the PV industry then, the only reason further declines have not been seen is largely due to the actions (a combination of pro-active and enforced measures) of the Chinese PV manufacturing sector; such as eliminating all non-essential spend (in particular capex), offloading any non-core operations (such as subsidiaries or held assets such as PV power plants), headcount reductions, retiring outdated capacity, renegotiating energy supply contracts, and squeezing suppliers (where possible).

An additional (and most welcome) factor for the polysilicon segment in China has been a meaningful uptick in pricing, that has greatly helped the rate of loss-making decline in this segment. However, the pricing uptick here must be seen in isolation due to the severity of the pricing declines seen for polysilicon suppliers in the past few years. More importantly – and pertinent within the context of the new research in this article – is that the uptick seen by the polysilicon suppliers has not been beneficial to the industry as a whole and has not allowed for similar related price increases from a global module standpoint. In fact, downstream channels have had to absorb this increase in polysilicon ASPs as a higher direct materials cost.

From an enforcement standpoint, it should be noted that – during the past 12 months – many PV manufacturing companies in China (through the value- and supply-chains) have been forced (by banks/lenders or through regulatory listing requirements) into insolvency proceedings (or related ‘restructuring’ by state-operated holdings that re-organize ‘zombie’ operations). This has had the effect of ‘correcting’ the segment in sorts, writing off some bad debt and averting ongoing operational losses (and by default sales losses) from these shuttered factories.

However, the main takeaway so far is that the PV manufacturing segment has likely passed through the Downturn Trough and is officially in a ‘recovery’ transition phase, something that is necessary before the end of the downturn can be called; the Margin Recovery period shown in Figure 1.

Forecasting the next 12 months is still challenging, as the PV sector’s end-market is ‘sluggish’, highlighted by the likely year-on-year decline in productivity levels and a fall in installed PV system capacity globally in 2025.

The graph in Figure 1 shows three forecasted scenarios (labelled as Rapid Rebound, Ideal Trajectory and Slow Recovery) needed to reach the end of the downturn. The range of end points is illustrated as the Downturn End Zone.

Downturn is U-shaped, double-dip can’t be discounted yet

So far, the second PV manufacturing downturn has proceeded as a single ‘U-shaped’ phenomenon, characterized by a steep decline into the downturn (the sharp recessionary element) and the lack of a clearly defined trough (replaced by a prolonged period of stagnation over several quarters).

U-shaped downturns typically have different outcomes, compared to the more familiar V-shaped events. U-shaped downturns tend to have a slower recovery (as opposed to the shallow V-shaped bounce-back that occurred during the first PV manufacturing downturn of 2012-2014).

Now, this may seem a bad thing for the PV industry, but here is why I think it is better if the recovery from the downturn takes longer.

U-shaped downturns tend to have a more ‘lasting’ recovery than V-shaped ones, with the learnings (cost-reduction exercises, supply-chain corrections, technology-choices, greater prudence in taking on new debt to invest in expansions) being ones that simply would not have been undertaken had the recovery been a bounce-back effect.

Indeed, the solar industry probably needed a severe U-shaped downturn to stop the reckless capex climate that was created by years of seemingly invincible ‘growth-with-profitability’ between 2015 and 2023.

The three recovery scenarios forecast an end to the current downturn between Q2’26 and Q4’26, with the quick-wins (strong recovery growth since Q2’25) being replaced during Q4’25-Q1’26 by slow-but-steady recovery.

Furthermore, at the end of Q4’25, reporting will likely be skewed by impairment charges and divesting more non-core assets; and Q1 is notoriously a slow quarter for the PV industry when inventory is accumulated.

Therefore, the model here suggests that the end point of the downturn will be mid-to-late 2026.

If the Rapid Rebound trajectory is seen, there is a strong risk of misplaced spending returning to certain parts of the sector, only to see a recurrence of loss-making within a couple of years. The Ideal Trajectory or Slow Recovery options have a much greater chance of lessons being learned going forward.

However, the main concern right now is the risk of a double U-dip downturn event coming to fruition.

A double-dip could occur if the initial recovery is not sustainable, or if 2026 end-market demand is considerably on the low-side, creating another oversupply of modules and a new round of price wars to shift product. It could also happen, for example, if there is a surge of India-made modules hitting export market channels. But right now, let’s park the possibility of a double-dip and return only if signs emerge to warrant further discussion.

Recovery at the sub-system level

To understand how much work still needs to be done to restore gross margins through the value- and supply-chains, consider Figure 2 below. This shows the weighted contributions of the gross margin deviations (actual gross margins to target comfort zones), for each of the seven segments outlined above.

Starting top-left, this graph represents the landscape during 2020, with almost all the segments comfortably ‘over-performing’ relative to the target margin levels assigned in this research study. Fast forward to mid-2023 (top-right graph, just before the onset of the downturn) and margin compression is clear to see, with only polysilicon left to see final margin levels eroded.

Bottom-left shows the severity of the downturn, with the entire sector showing strong excess losses. The only segment that is structured to ‘evade’ overall sector trends is the metallization paste suppliers that, for many years (since paste supply leadership was transferred from DuPont and Heraeus to Chinese entities), have been the gold-standard for manufacturing in the PV industry; set up as processing ‘shops’ based on buying materials (mainly silver powder) at market value and selling with a prescribed delta. This feat is even more noteworthy, given the spot price increases in silver over the past couple of years.

The final graph (bottom-right) is from reporting over the past couple of weeks from the 21 companies analysed in the research, capturing Q3’25 metrics. This shows a decline in the level of losses, but still with some way to go in getting into the black.

What will 2027 look like? Will globalization of manufacturing create new dynamics?

The subtitle above is another of the sector’s big talking points today. From a research perspective, 2026 is largely a year of recovery. The big question is – what happens in 2027, assuming the downturn is over?

If the recovery is not a double-dip event and follows the Ideal or Slow recovery paths (as shown in Figure 1), 2027 could be a landmark year for the industry – if the lessons of the downturn are adhered to (in particular, an end to capacity expansion in blind faith).

However, a return to capacity investments may not even come into the equation if end-market demand remains ‘constrained’, with more than enough installed (and state-of-the-art) capacity in place now to serve a modest-growth industry out to 2028; especially if one factors in the circa. 50 GW worth of new/mothballed capacity through the system in China today that will likely be consumed by existing players if new capacity is needed at short notice.

Rather, the uptick in capex (outside of activity in the U.S., India and the MEA region) that is characteristic of a new upturn cycle could be dominated by upgrades to existing capacities or from a new technology buying cycle (as would happen, for example, if full back-contact technology gains strong traction in 2027).

However, the big worry is that the sector fails to learn from previous mistakes, in terms of being too fragmented across the value- and supply-chains; and having certain parts of the manufacturing system that ‘hoard’ profits at the expense of an overall healthy sector.

There are about 150 entities today (covering PV manufacturing and materials supply) that have meaningful capacity levels. While competition between companies at specific value-chain or materials-supply segments is ‘healthy’, the problem arises when there is competition between these segments to hoard profits at the expense of others.

One can see this today with the China polysilicon ‘consortium’ of key producers seeking to restore a legacy manufacturing era in which the profitability of these companies was at the expense of other segments and created an unbalanced sector that was incapable of preventing a deep dive into recession.

Perhaps China needs industry directives to the entire sector that curb excessive profiteering (as opposed to a focus on new capacity or market pricing guidelines) and a plan for the China PV industry to recover as a whole – not left to individual segments to claw their way out of the downturn in isolation.

Of course, it should be the sector itself that corrects its modus operandi going forward, not the government. But the continued fragmentation and sheer number of companies in the system makes this extremely difficult to do in practice.

The only hope would be that five companies (namely Jinko, LONGi, JA Solar, Trina Solar and Tongwei) form an ‘alliance’ of sorts that targets profit margin levels to be set and maintained by all segments of manufacturing/supply; this then becoming a ‘standard’ that all manufacturers in China adhere to, in a way that only paste suppliers have been subjected to until now.

To explain this in another way, consider this.

If any single company in the PV manufacturing segment was fully vertically-integrated (value and supply-chains, either in-house owned or with an effective fab-lite/fabless mantra, with dominant market-share status for each segment), it would not be permitted for different business units to profit at the expense of others, or to hold other parts of the company to ‘ransom’ in supply-constrained periods.

It is a tall challenge of course and history is not on the side of manufacturing in the PV industry, with the two downturns until now having been clearly signposted well in advance.

The other option is to deny everything and pray for product pricing to miraculously double in the next 18 months! Downturn? What downturn? Stranger things have happened.

Or to be so entrenched in a different part of the world (not China) where other factors are in place – such as seems to be the case today in the U.S. and India.

On this note, let’s close out the article with what this all means for the manufacturing plans of companies active in the U.S. and India today, or those looking to get into PV manufacturing in the next 12-18 months.

Incentives are good to kick-start activities, but what next?

It is fascinating today to see the different levels of confidence between Chinese PV manufacturers and suppliers (that still account for well over 90% of everything produced) and existing/prospective manufacturing entities in the U.S. and India.

Is this really the same sector?

Relying on government-enforced manufacturing incentives and import restrictions on competing products is tactical, not strategic. Relying on a single domestic market for sales is equally precarious.

Yet, the rhetoric in the U.S. and India for domestic manufacturing remains extremely bullish. Optimism in India appears to be at an all-time high regarding PV manufacturing, with the success of Waaree’s 2024 IPO placement being a major catalyst in this regard.

Each of these countries is not new to PV manufacturing investment phases. India is currently in its third phase to onshore cell manufacturing. The U.S. is now being pushed and pulled by foreign-entity based concerns, driving a must-make-everything-tomorrow approach across a highly fragmented manufacturing landscape; this coming after three decades of false starts and speculative technology punts.

During the past few years, India has had only one credible export market (the U.S.). Manufacturing in the U.S. has next-to-zero prospects of being an export industry, today or tomorrow.

Indeed, if the door fully closes on Indian companies exporting to the U.S., then the two regions where manufacturing has a protective framework in place (India and the U.S.) would simply be self-serving landscapes, fully dependent on localized end-market pulls.

Ultimately, with or without incentives or competition from imports, factory yield and profits will be the only metrics of value. At some point in the next 18 months, the focus will move away from capacity-announcement euphoria to profit-counting reality in the U.S. and India.

And it should be remembered that only one U.S. manufacturing company has succeeded in the PV industry until now – First Solar; a company with a differentiated technology and supply-chain to all other companies in the industry.

However, all said and done, 2027 (not 2026) is going to be a massive year for the PV industry.

Can China recover and learn from previous over-investment and localized profiteering? Can c-Si PV manufacturing in the U.S. and India be profitable and develop a plan to exist in the absence of domestic incentives?

Factoring in also the developments (manufacturing capex) today in the MEA region, PV manufacturing in 2027 will certainly look way more global than a few years ago when almost everything was made in China or by Chinese-owned subsidiary operations in Southeast Asia.

Ultimately, this is something to celebrate regardless of how, or why, the factory investments came to fruition. But let’s wait and see who makes money out of this and which companies have a credible long-term business plan going forward.

When the third PV manufacturing downturn does inevitably happen in the future, let’s hope that companies are better prepared individually and more organized as a collective unit.