Throughout almost the entire history of the solar PV industry, the ingot and wafer stages of the c-Si value-chain have been rather neglected in coverage and scrutiny, compared to the production of polysilicon, the fabrication of cells and module assembly.

However, as a key part of the upstream c-Si value-chain, it has become increasingly important in the past few years to understand where ingots and wafers are being produced, and by whom. This shift is coming from the new focus on supply-chains and traceability of upstream component origin.

This blog takes a new look at ingot and wafer production in the PV industry since the start of this decade (from 2020).

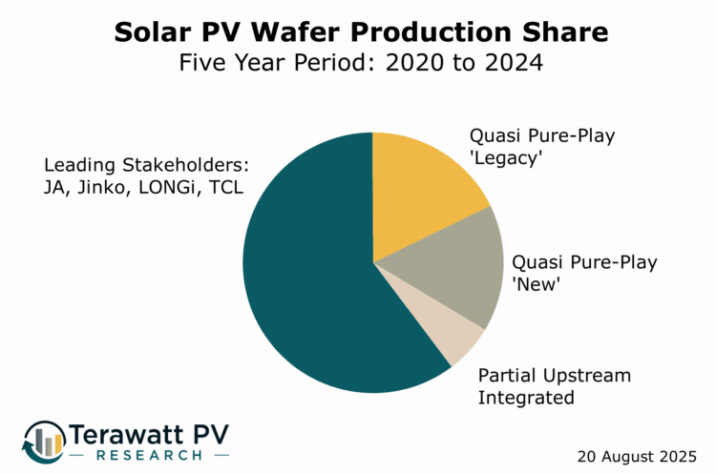

Specifically, all wafer producers are segmented into just three main categories: Leading Stakeholders, Quasi Pure-Play and Partial Upstream Integrated. The Quasi Pure-Play category is divided into ‘New’ entrants since 2020 and ‘Legacy’ producers that were prominent before this time.

The output (shown in the graphic above) reveals the dominance of just four companies forming the Leading Stakeholders; JA Solar, Jinko Solar, LONGi and TCL Zhonghuan. These companies have produced about 60% of all wafers made in the solar PV industry in the past five years. The remaining contribution to wafer production is mainly coming from Quasi Pure-Play manufacturers (circa. one-third of production).

The Leading Stakeholders category

Just 15 companies are responsible for more than 95% of all wafer production in the PV industry over the past five years; an incredible statistic given all the announcements made during this period from companies looking to enter the industry or expand upstream.

Furthermore, four of these companies (JA Solar, Jinko Solar, LONGi and TCL Zhonghuan) are the clear drivers in terms of production volumes and sector influence, responsible for about 60% of all wafers produced since 2020.

While LONGi and Zhonghuan come from pure-play wafer backgrounds (from a market-entry play perspective), JA Solar and Jinko have consistently been the two entities that have embraced vertical-integration (ingot-to-module) as a strategic means to retain technology leadership (mainly at the cell level).

The LONGi of today is a very different entity that came to prominence about 15 years ago with the slogan ‘mono is the future’. Wafer revenues are still important to the company, but the focus today is selling modules (as a globally recognized brand); and recently being a frontrunner in driving cell technology change out to 2030.

For years a China-centric player in PV, TCL has routinely sought to broaden its value-added proposition in the sector, most noticeably through its investments in SunPower (and subsequently Maxeon). TCL Zhonghuan is one of a group of companies (in the broader PV manufacturing universe) that ultimately has ‘parent-company’ security.

While LONGi, TCL, and the pairing of JA Solar and Jinko, may appear to have somewhat different operating goals, these four companies are the clear leaders in wafer production since 2020 and share a wafer-play-prioritization that differentiates them from all other wafer producers in the industry. As such, these four companies form the grouping of Leading Stakeholders, responsible for 60% of all PV wafer production in the past five years.

The Quasi Pure-Play category

The next category of wafer producers is comprised of companies (or autonomous subsidiary operations of larger PV entities) that have been created, or have sustained operations, to serve PV cell demand, rather than be agents of change.

The nomenclature assigned to this grouping is Quasi Pure-Play, as none of the companies is an ingot/wafer pure-play operations in the classic sense; rather, each company typically has adjacent or legacy revenue streams, often from an equipment standpoint (e.g. pullers or wire saws).

Indeed, many of these companies have tried to expand downstream to cells or modules (with varying degrees of success), but their raison d’être in PV is rooted in making ingots and/or wafers. Hence the prefix of Quasi being applied here.

Within the context of the timelines being reviewed in this blog (the five-year period from 2020 to 2024), this Quasi Pure-Play grouping can be further segmented by market-entry timing.

Companies active in the sector prior to 2020 are termed Quasi Pure-Play ‘Legacy’; this includes the likes of Hongyuan, Jingyuntong and Meike.

Companies new to the sector in the past five years are labelled as Quasi Pure-Play ‘New’, such as Shuangliang and Gokin.

This group of companies has made the wafer production landscape more diversified today, compared to 2020 (and some years before when LONGi and Zhonghuan were producing more wafers than all other companies added together).

However, market-entry timing did not offer any favours to these companies with funding models of the early 2020’s being subjected to the depressed pricing environment ushered in by the manufacturing downturn at the end of 2023; precisely the point that many of these new entrants had ramped up capacity that was financed back in 2021 and 2022.

The Partial Upstream Integrated category

The final grouping is comprised mainly of known global module suppliers that have varying degrees of ingot, wafer and cell capacity in-house, but rely to a large part on outsourcing wafers or cells from third parties.

Currently, the most notable inclusions here are Trina Solar and Canadian Solar (through its CSI Solar operations). However, over the years, many companies (again mostly driven by increased upstream flexibility) have come in and out of this category; not to mention the huge number that included wafering in original funding plans, but chose to install cell and module capacity, or simply assemble modules buying in cells.

Each of these companies tends to operate a flexible vertical integration model, choosing when to step up or down the portion of in-house production (at cell and wafer stages). Decision-making here often comes from pricing and availability from other wafer producers (typically the Quasi Pure-Play companies) at any given time, in response to technology changes that may render existing ingot/wafer capacity obsolete (seen in the past in the move from casting to pulling ingots), or as a direct result of supply-chain scrutiny (as witnessed today from traceability concerns).

Evolution of wafer landscape going forward

Investments into ingot and wafer facilities in China have been extensive in the past few years and it is unlikely any major capacity additions will be needed in the short-term.

New capacity (at significantly lower capacity levels) is likely to emerge outside China and Southeast Asia; India, the MEA region and in the U.S. However, Chinese companies are responsible for more than 99% of all wafer production today and this is not likely to change going forward (for a host or reasons).

In terms of key sector dynamics, the most interesting one to watch could be based on the fate of the Quasi Pure-Play ‘New’ companies and whether profitability can be restored in the near-term.

Equipped with current state-of-the-art pullers and wire saws, the facilities owned by these companies (specifically selected subsidiary operations) could be prime for acquisition in 2026 or 2027 when some of the Leading Stakeholders or Partial Upstream Integrated producers plan their next capex and expansion cycles; or simply taking over stranded assets or as part of debt-to-equity arrangements.

Over the next six months however, all eyes are on cost reduction and returning to profitability, like much of the PV manufacturing sector in China today.