Debt and cash-flow problems continue to hamper the operations of almost the entire Chinese solar PV sector, with green shoots to signal the end of the downturn nowhere to be seen.

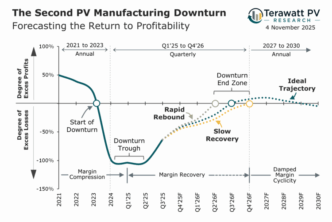

The second major PV manufacturing downturn, that started towards the end of 2023, sees no signs of rebounding during 2025. Indeed, it now appears that 2026, not 2025, is likely to be the year of recovery, with 2027 being the start of a new paradigm in commoditized high-volume mass production.

Underpinning this outlook is a new examination of the entire eco-system upon which the Chinese solar PV manufacturing sector is now reliant on; in particular, the companies making the key components through the c-Si value chain (polysilicon, ingot, wafer, cell and module) and their material suppliers that are the dominant contributors to the direct materials costs in production.

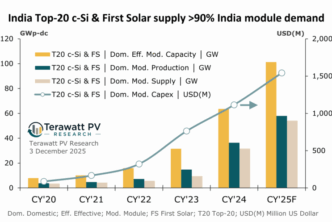

With India and the U.S. pre-occupied with capacity announcements and using domestic incentives to counter global manufacturing benchmarks, how China re-orders its c-Si sector will ultimately determine the success of solar PV manufacturing globally.

Reducing manufacturing costs now accepted as the only way to survive going forward

When the downturn set in at the start of 2024, many of the PV manufacturers of polysilicon through to modules simply hoped that pricing would rebound, allowing margins to be restored to legacy operating models that had existed prior to 2024.

However, by the start of 2025, a more pragmatic assessment was in evidence, with end-market demand for PV globally somewhat flatlining compared to the meteoric growth seen in previous years.

Confronted with the inevitable uptick in long-term debt obligations and the dwindling of cash reserves for day-to-day operations, most PV manufacturers in China ended their fixation on new capacity additions and focused on selling non-essential assets to shore up their balance sheets.

However, this did not address the fact that production costs were still too high, given that the pricing through the value-chain had not seen any meaningful rebound.

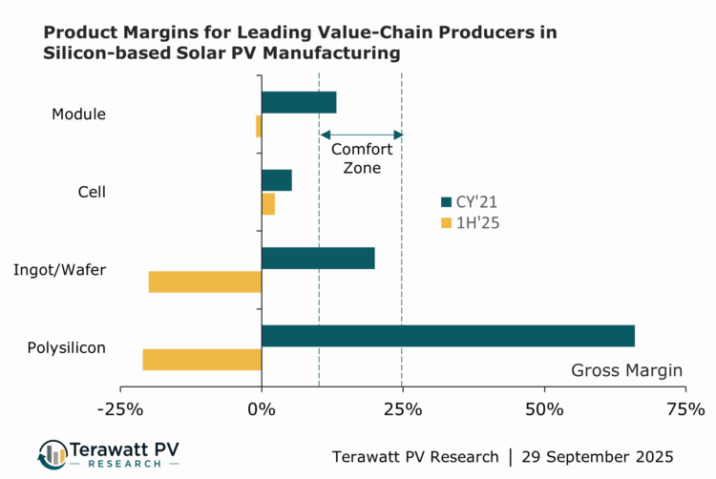

Figure 1 (above) shows how much production margins have been eroded through the value-chain during the downturn. Component-specific revenues and costs from the value-chain production leaders (for each of polysilicon, ingot/wafer, cell and module) have been consolidated for operations during the first six months of 2025 (1H’25) and compared to the full calendar year 2021 (CY’21), when the sector was last in growth mode with positive metrics.

Comparing the relative fortunes of the leading producers through the c-Si value-chain, polysilicon suppliers have been impacted the most. This is not altogether surprising, given that polysilicon supply was the gating factor in the overall supply/demand balance to the sector until the end of 2023. Indeed, this explains why the Chinese polysilicon community has been the most vocal in the past 12 months about creating an artificial mechanism to set a base pricing in China that would assist in restoring profitability for the market leaders.

However, as is explained further below, what the polysilicon sector in China is really advocating is for module sales prices to be increased (given the lack of ‘give’ anywhere else in the value-chain and from materials suppliers). Perhaps, it is simply a case of comeuppance for the leading polysilicon suppliers in China, given their propensity in the past to stack sector profits in their favour when end-market demand exceeded supply.

Certainly, from a value-chain perspective, there is no give at ingot, wafer, cell and module stages. Moreover, many companies here are living in hope still that upstream pricing will rebound, allowing them to increase prices. Therefore, any price uptick in the value-chain will have to be absorbed by way of higher module prices, something that is only in evidence today in the U.S. and India (and subject to regional outliers and caveats that are not helping Chinese domestic production).

Is there slack in materials costs to overall COGS stacks?

During the previous (or ‘first’) PV manufacturing downturn (2012-2014), the Chinese sector was able to navigate back to profitability largely by focusing on cost reduction efforts that were absorbed by the actions of their key materials suppliers.

Indeed, it was the success of this consolidated process that largely saw the removal of Western competition (Japan, South Korea and Europe) to Chinese PV manufacturing; in particular, for materials supply at all stages through the c-Si value-chain.

In fact, one could argue that the actions of the Chinese sector to reduce costs back in 2013 was the catalyst in creating a near-complete c-Si manufacturing eco-system that then allowed technology advances to be implemented at rapid pace.

So, the obvious question to ask now is whether producers of say, wafers cells and modules, can squeeze their materials suppliers once again?

The answer to this is a resounding ‘no’ and forms the basis of the forecast now that the downturn is set to last through most of 2026 and possibly even into 2027.

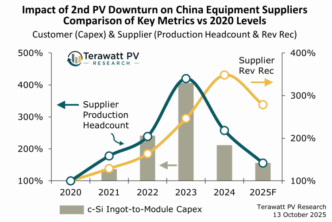

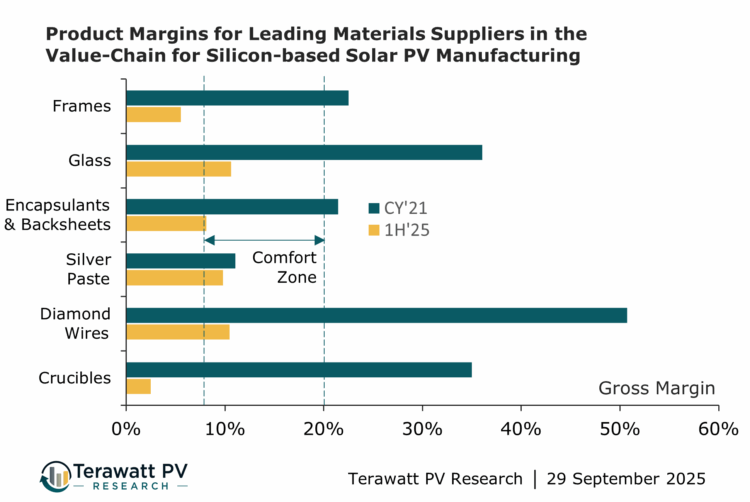

Figure 2 below features suppliers of the key contributions to the COGS through the value-chain in making ingots (crucibles), wafers (diamond wires), cells (metallization paste) and modules (films, glass and frames). Again, comparison is shown for CY’21 and 1H’25, by consolidating the PV component-specific revenues and costs for the leading PV materials suppliers today for crucibles, diamond wires, pastes, films, glass and frames.

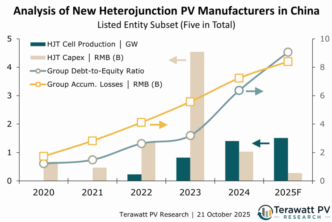

Except for the leading paste suppliers, all other leading materials suppliers have seen margins eroded in a similar way to their customers (ingot, wafer and cell module producers). For many of these companies (that became materials supply leaders after the 2012-2014 downturn), this is the first experience of negative operating losses.

Clearly though, the idea that wafer, cell and module suppliers can expect their materials suppliers (that typically account for 70-90% of total COGS) to reduce pricing further, to help them restore margins, is not viable.

Indeed, all materials suppliers (apart from the leading paste suppliers) now find themselves with the same problem confronting their customers – how to reduce costs.

However, this is where the problem kicks in for the solar PV eco-system today; materials suppliers’ COGS are themselves similarly weighted (80-90% plus) by direct materials but these follow stock price indices of raw material commodities.

Has the material age of solar PV manufacturing started now?

Unless global solar module pricing doubles (as a minimum, and excluding the price outliers today in the U.S. and India) in the next 12 months, and stays at these levels, it could be that the sector has hit manufacturing cost dynamics that were not expected to kick in until the early 2030’s when the sector was at multi-terawatt production levels.

Specifically, has the industry (at least from a Chinese manufacturing perspective) entered an era of modules being sold at a level where costs through the entire value-chain are dominated (at the 70-80% level) by commodity pricing outside the control of the sector?

Could this account for the somewhat confusion that seems to be in evidence today as component suppliers appear to simply continue operations without any clear plan of how to return to profitability (other than the hope of the polysilicon suppliers that the rest of the sector will happily go along with their price uptick aspirations to aid their own plight)?

There is one main factor however that may reverse this sudden and apparent race-to-the-bottom landscape – supply/demand dynamics through the value-chain. Essentially, is there any prospect of a supply bottleneck that will ultimately feed into a module supply shortage? Like the factors that are bumping up prices for module supply to India and the U.S. (that have localized shortage dynamics).

From a China c-Si perspective, having a wafer, cell or module supply-shortage is highly unlikely, given the country’s ability to bring 10-20 GW fabs online in a matter of months if essential. Therefore, polysilicon supply looks like the only option, with an ‘act of God’ – that takes multiple sites out of operation for an extended period – being a more likely catalyst than the market leaders today being successful in forming a meaningful cartel in China.

My initial take is that the ‘materials age’ has indeed arrived and that this is spooking the sector globally (not simply China) without many accepting this new reality. In fact, many PV stakeholders outside China don’t care too much, as most are buying modules and have got used to price levels over the past 12-18 months.

And while proponents of PV manufacturing in the U.S. and India may cling to the notion that they can succeed on their own terms, the reality is that the U.S. and India need the Chinese PV manufacturing sector to recover during 2026 if they are to stand any chance of creating a value-added domestic eco-system over the coming decade.

What does 2026 look like?

Assuming no major changes in 2026 compared to 2025, margin recovery through the value-chain (and down through materials suppliers) will have no silver bullet to rescue the entire sector. This also assumes there is no major technological breakthrough that would have an instant (and positive) effect for all manufacturing stakeholders.

The way Chinese PV manufacturing recovers then becomes a sum-of-moving-parts project, where pounds are saved by removing pennies everywhere possible. And with solar PV being a RMB/Wp ratio play, this promotes decreasing material usage rates (or indeed using different materials altogether) while retaining module efficiency levels (or even squeezing out miniscule enhancements step-by-step).

If this is what 2026 has in store, the impact on manufacturing will be profound and far more than just watching a series of tiny cost-savings add up over the year. More on this in a separate blog in the coming days.

Regardless of how the sector pans out in the coming 12 months, the notion of there being some green shoots emerging that would signal that the downturn was in sight can be parked for now. Chinese PV manufacturing is facing its biggest challenge yet and needs to consolidate a recovery plan now that benefits the entire sector, not simply the stage of the value-chain or material-type that the individual companies focus on.

To devise a recovery plan that is indeed sector-generic, it is necessary to have the collective buy-in and agreement of the root problem in the first place from the key participants. There is no evidence that the Chinese PV sector has got to this stage today, at least from the perspective of the industry ‘guidelines’ that are issued from central government in terms of ‘recommended’ business practice.

In the absence of being somewhat ‘ordered’ what to do in 2026, it then comes down to a survival-of-the-fittest mentality at the company-level that ultimately allows the group (sector) to prosper collectively. Either way, the term ‘cost-reduction’ will continue to be the manufacturing metric most discussed by component and materials suppliers to the end of 2025 and for most of 2026.