Since I started writing solar photovoltaic (PV) market reports more than 15 years ago, downstream industry stakeholders have broadened their reach in terms of outsourced intelligence requirements.

Gone largely are the days of market reports confined purely to technology shifts or near-term pricing indices. Rather, demand has turned to understanding manufacturers throughout the value chain; corporate ownership status, manufacturing bases operating globally, specific productivity, security of supply-chains, financial stability and ESG credentials.

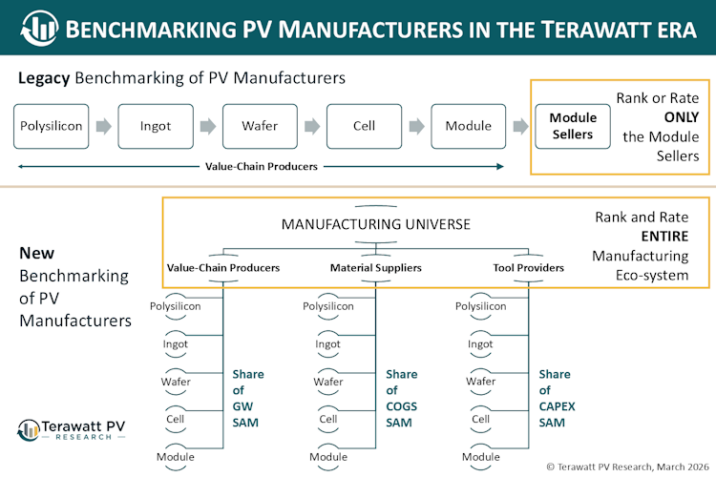

Moreover, the days of focusing mainly on module suppliers, or relying on claims from this one part of the overall eco-system, are rapidly disappearing.

Over the past few months, I have spent considerable time working out what a new solar PV market research report should look like; a report matching not just current demands from the industry, but one that reflects the trends that will become even more important over the next decade. This demanded a new methodology.

New methodology – a 360 degree look at the manufacturing eco-system

A recurring interest for 20 years has been factory productivity across the value-chain; polysilicon, ingot, wafer, cell and module. Additionally, during my formative years looking at the solar industry, there was a strong focus on the companies supplying the production equipment and materials for PV fabs.

Fast-forward to 2026 and it’s a return to this fascination of sorts – once again broadening the coverage beyond the companies producing polysilicon, ingots, wafers, cells and modules, and mapping out the market share contributions also of the materials suppliers (from quartz crucibles to solar glass) and the production equipment providers (serving capital expenditure, or capex, spending).

This has widened the pool of players in the universe somewhat but has offered a deeper understanding of the entire manufacturing eco-system today; in particular, the key strategic and supplier arrangements that are critical to the continued success of many leading industry companies today, and exactly how technology is evolving.

Crucially, this approach enabled a long-standing research goal to be achieved: mapping out the relative manufacturing eco-system status – or standing – of all meaningful companies within the PV manufacturing industry. A far cry from simply ranking companies by module shipment volumes or looking at just one part of the value- or supply-chain in isolation, such as polysilicon.

Today, about 120-130 companies manufacture more than 98-99% of all polysilicon, ingots, wafers, cells, modules, key materials/consumables (e.g. crucibles, diamond wires, metallization pastes, films/backsheets and glass) and factory production equipment (including, for example, ingot pullers, diamond wire saws, cell process tools and module assembly equipment).

But what if the business model of each of these companies in the entire eco-system could be scrutinized in detail and benchmarked? Not simply the headline numbers the companies promote to the outside world – but analysing each company and understanding the strategies at play in terms of ongoing operations and competitiveness.

The three pillars of PV manufacturing performance

Today’s scrutiny on companies manufacturing in the solar PV eco-system falls broadly across three main categories, or pillars.

First, the above-mentioned productivity levels – which companies command the leading market shares at every stage of the value- and supply-chains.

Fundamentally, manufacturing is about production – not simply looking at module shipment volumes (part of which many companies don’t even produce themselves) or capacity announcements. Nor is manufacturing about “ignoring” upstream value-chain production or the entire materials and equipment supply sectors.

Every company in the PV manufacturing eco-system commands a specific market-share. Some have contributions by making different elements; cells and modules, polysilicon and modules, modules and encapsulants or frames, diamond wire saws and diamond wire consumables, ingot pullers and ingot production.

I remember years ago being told to avoid even trying to benchmark c-Si and thin-film module producers! Like these were analogous to apples-and-oranges. But this rather blinkered approach stems from a legacy sector fixation with looking only at a simple value-chain of component producers and over-emphasizing the value of final module shipment or selling.

The new methodology unpinning the “manufacturing” aspect of the analysis considers the PV manufacturing space as a summation of “stages” where companies can do (at least) one of three things: supply the production equipment (e.g. a deposition tool or a stringer), provide the raw materials (e.g. the silver paste or the glass), or manufacture the finish goods (e.g. a wafer or a module).

Envisaged as a collection of multiple served addressable markets (SAMs), each is made up of market-share contributions: output of the wafer producers (in a GW-world), supply volumes of the materials suppliers (a function of cost of goods, or COGS), and capital expenditure (capex) allocations for the tool suppliers.

As such, within the whole PV manufacturing eco-system, the productivity of all its contributors can be benchmarked purely from a quantitative standpoint, numbers-driven, and coming from market-share reality at any given time.

The second key pillar of “manufacturing performance” relates to financial health. This is a much easier process in terms of benchmarking as there is – of course – nothing differentiating company accounts from a value- or supply-chain perspective.

The challenge here, however. was to find a robust means of comparing the financial metrics of companies specific to the PV industry, allowing direct comparison of public and privately held entities, and dealing with PV manufacturers that were part of large well-capitalized “conglomerates”.

More on this in the coming weeks. And how the research phase for the new report required going back to basics on financial auditing and understanding which accounting ratios offered the greatest insight into PV manufacturers from an ongoing operations perspective.

The third key pillar is based on a new performance metric that has emerged in recent times, relating to corporate governance, transparency, supply-chain visibility, and a host of interrelated factors that fundamentally sit under a broader heading of “Corporate Transparency”.

Essentially, my thinking on this was that “traceability” per se is just a one part of a bigger issue that should be called “transparency”. And this “transparency” today cannot be in stealth, rather as open disclosure. Full details on the methodology for this – the most qualitative across all the key pillars – will be outlined shortly.

In summary, a new methodology has been established to ultimately benchmark companies across the entire PV manufacturing eco-system – the three pillars of production, finance and transparency. A process that essentially reveals the companies holding the fabric of PV manufacturing together. The companies that routinely show up in module factory audits. And the equipment providers that are often the technology- and yield-enablers of the PV industry’s participants.

Once the new report is released on 26 March 2026, I will go into greater detail regarding the methodology and validation. And, of course, what this means for all the companies we read and hear about so much every day in the solar industry. The best way to flag interest is the new report is to send an email to: contact@terawatt-pv.com.