Four years ago, researchers at Sheffield Hallam University released a report on upstream (mainly polysilicon) solar supply chains in China. The findings set off a chain reaction in the solar PV industry that brought traceability to a new audience (mainly module buyers) hitherto not required to scrutinise upstream component manufacturers and production locations within China.

A key topic within my ongoing book-writing research phase is the dynamics of the polysilicon segment (from the early days of buying scrap material from semiconductor grade producers to solar-grade specific facilities of 100,000-200,000 MT capacity being constructed in China).

This topic has been instrumental to the fortunes of almost all stakeholders within the industry over the past few decades.

There have been several phases that solar polysilicon manufacturing has gone through in the past 20-30 years. Until 2021, such periods were often characterised by under and over-supply, and the impact this had on midstream manufacturing profitability and end-market growth metrics.

However, since 2021, following the Sheffield Hallam report (and subsequent trade-related policy decision-making by U.S. government agencies, and evolving corporate ESG buying practices), manufacturing locations and supply-channels (inbound from industrial grade silicon refining and quartz sand mining, and shipping to ingot pullers and their customers through to module assembly) have become the dominant issues to track.

Between 2020 (the data collection year for the Sheffield Hallam contents) and 2024, the solar PV industry has seen robust end-market growth, with polysilicon production levels some 3-4 times higher in 2024 compared to 2020. This five-year period has seen the extremes in operational performance from polysilicon producers being reported, including back-to-back phases of record profits and losses.

During this five-year period, polysilicon investment exuberance has also been to the fore in China, on a level not seen previously (even by China solar standards). Barely a day passed during 2021 and 2022 without a new polysilicon ‘project’ (often linked to industrial grade silicon investment plans) being unveiled.

These project plans came from a wide range of stakeholders; new companies formed typically by personnel with legacy leadership positions at incumbent polysilicon entities, existing polysilicon suppliers seeking to increase market-share allocations, and established organisations (often provincial industrial entities under state-ownership) seeking to diversify into a new ‘green economy’.

Hundreds of memoranda-themed handshakes were captured on camera (often with local officials), in addition to endless ribbon-cutting, ground-breaking ceremonies. (Not to mention a steady flow of social media ad-hoc commentary on possible investments into the sector.)

So, five years on from 2020, what has really happened? And more importantly, how has polysilicon production in China changed since the Sheffield Hallam report? This article addresses this question.

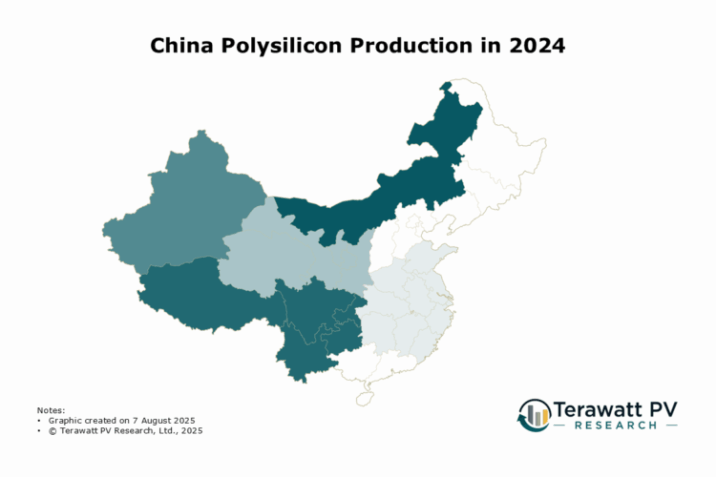

Xinjiang polysilicon production 80% higher in 2024, compared to 2020

Figure 1 below shows a solar polysilicon production ‘heatmap’ for China, comparing volumes in 2020 and 2024. The key feature to this new analysis is the focus on production, not capacity. Adding up capacity announcements can easily mislead the findings, based on the number of polysilicon facilities that have been operating at reduced rates or shuttered since the start of 2023; not to mention new facilities that were half-built, or built and not moved into production (somewhat of ‘white elephant’ status).

Segmentation by province or geographic region is critical to fully understand the changing production landscape between 2020 and 2024. In this context, Xinjiang and Inner Mongolia are the only two provinces that are shown directly. The rest of Northwest China (mainly Ningxia and Qinghai and excluding Xinjiang) is then broken out for representation.

Southwest China is highlighted as the next key province, dominated by production in Sichuan and Yunnan. Finally, East China and Central China are grouped together, due to geographic proximity and relatively low contributions to the overall polysilicon production volumes in China over the period in question (2020 to 2024).

Therefore, five areas are segmented to best illustrate the production trends: Xinjiang, Inner Mongolia, Southwest China, Northwest China (excluding Xinjiang) and East & Central China.

Showing the production heatmaps side-by-side provides the basis for the commentary now.

The first takeaway is pure volume based. Chinese companies’ contribution to global polysilicon supply increased from circa. 80% in 2020 to over 95% in 2024, at a time the end-market supply of modules increased by more than 3X. Therefore, it is not surprising that volumes in almost all the five key areas (except for East & Central China) show strong production growth levels.

However, the main difference between China polysilicon production in 2020 and 2024 relates to the geographic share allocations across Northwest China, Inner Mongolia and Southwest China.

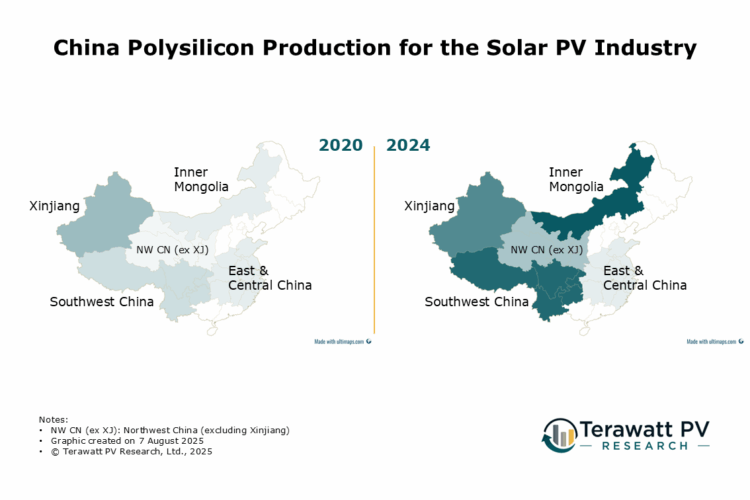

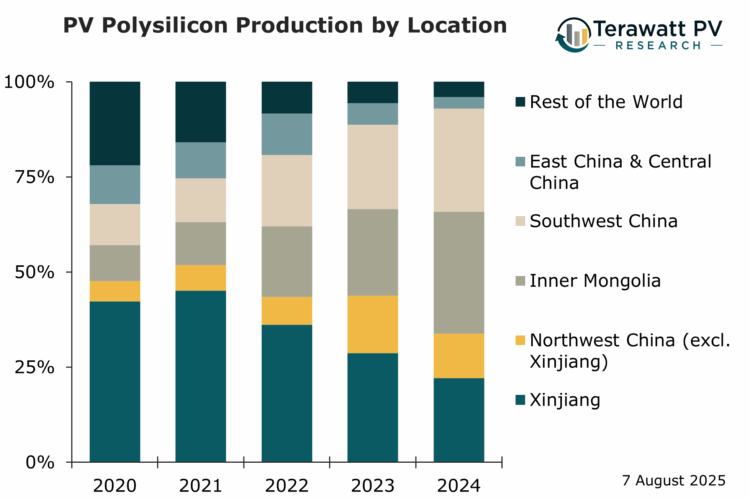

To understand this more clearly, Figure 2 below tracks the contributions (polysilicon production) from all five segmented areas by year from 2020 to 2024, including also solar specific polysilicon production from the Rest-of-the-World (Malaysia, Germany and the U.S.).

This figure confirms the segmentation rationale outlined earlier and why it is important to treat Xinjiang and Inner Mongolia on a stand-alone basis.

Looking at the production share by area by year, it would be easy to conclude that there was a ‘move’ of sorts from Xinjiang to Inner Mongolia for polysilicon production, but one needs to consider raw production numbers, something that the production heatmap in Figure 1 shows clearly.

Polysilicon volumes from Inner Mongolia increased more than ten-fold in 2024 compared to 2020, driven mainly by new capacity ramped up by Daqo, GCL Technology, Tongwei and Xinte.

However, Xinjiang production volumes almost doubled between 2020 and 2024, with three of the five leading producers here responsible for more than 300,000 MT of new polysilicon capacity in Xinjiang during this period.

The reality is that polysilicon production in China has merely undergone a minor re-order in geographic location between 2020 and 2024. The share of polysilicon production from just five provinces (Xinjiang, Inner Mongolia, Qinghai, Sichuan and Yunnan) has been consistently in the range 85-90% each year from 2020 to 2024, and this is unlikely to change in the near to mid-term.

Stop-bleeding-cash the only focus today and tomorrow

It is unclear just how much money was lost in China in 2024 through polysilicon operations or simply squandered for a host of non-operational reasons. Production costs exceeded selling prices for most of the year, with massive inventory levels accumulated by year-end.

While the Western world (in particular, U.S. module buyers and downstream investors) focuses on scrutinizing polysilicon production locations in China and supply-chains from these facilities, the 10-15 polysilicon suppliers today in China are simply focused on halting operating losses.

For all these polysilicon entities, this largely means cost-reduction efforts, with energy prices from provincial suppliers being the one main contribution to production costs that can be re-negotiated.

Efforts are also ongoing to have a minimum pricing arrangement between suppliers; however, this requires everyone ‘playing ball’, something that Chinese companies have not excelled at in the past. Indeed, the suggestion that Chinese polysilicon companies could act like a single entity (or cartel) has been shown to be far-fetched in the past, characterised by a lack of collective strategy that could have kept supply tight a few years ago and prices elevated.

Rather, polysilicon manufacturers in China tend to act in their self-interest, often at the expense of others; or simply come from different backgrounds. Ultimately, this leads to a fragmented manufacturing landscape that routinely self-implodes.

To fully understand this – and to frame the current plight of the Chinese polysilicon sector – it is necessary to consider the different profiles of the 10-15 entities that are affected today.

The companies can generally be divided into three types; near-pure-play entities that have been supplying the sector for many years and have navigated through cyclical supply/demand phases before; subsidiary operations of well capitalized state-owned industrial ‘conglomerates’; and new entrants in the past few years that benefited from private placements through Series A and B funding rounds to enable upfront capital expenditure, motivated mainly by filing for an IPO in Shanghai, Shenzhen or Hong Kong in the future.

Polysilicon producers falling into the first two categories (near-pure-play incumbents and subsidiary operations of state-owned entities) are less impacted today by the low-pricing environment than the third category (new entrants backed by private equity).

The pure-play producers have generally built cash reserves from years of healthy profits and should be able to sustain losses in the near-term; furthermore, most have sufficient polysilicon capacity already and therefore do not need to raise new funds (through cash or debt) for any expansions or major upgrades (or indeed to shore up any potential working capital issues).

In fact, one should also remember that companies sometimes benefit from a depressed pricing environment, especially when competitors are losing even more money, or do not have sufficient reserves to sustain operations until margins return to positive territory. There are certainly some polysilicon suppliers that would benefit hugely if other producers were to exit the market, in the hope that gaining market-share would allow pricing to be controlled to a higher degree (perhaps if only through a return to supply tightness).

Producers operating as subsidiaries of large state-owned entities are largely shielded by parent company asset and turnover volumes, with the decision to continue in production (through a loss-making phase) being more strategic than tactical.

This leaves the debt-laden grouping of new polysilicon entrants as the entities at most risk today. Potentially sitting on stranded assets, offloading newly built plants may be the only exit strategy on the table. In fact, this could play nicely into the hands of the incumbents when, in a few years from now, extra capacity is needed to move to the next phase of growth.

Forecasting an uptick in polysilicon capex

Although the solar polysilicon sector (globally, not just in China) is currently haemorrhaging losses at record levels – and capacity expansion is the last item on board meeting agendas – it is nonetheless important to look into the future and consider when the solar industry will need more polysilicon capacity to meet market demand.

But therein lies the rub. Forecasting polysilicon demand is essentially a solar end-market deployment exercise in the next five years.

The question starts by asking how much the end market will grow in the next three years and comparing this to the likely effective polysilicon capacity that will be in the mix then (out of today’s operational, offline, and quality-sufficient built-not-ramped capacity).

As part of this exercise, it is also prudent to consider capacity that may be retired from existing polysilicon suppliers, for example; if Wacker was to pivot fully to the semiconductor at the start of 2026; OCI’s Malaysia plants were to be the focus of the company’s semi aspirations at the expense of the full JV with Tokuyama; or if Corning decided that a U.S. c-Si value-chain from ingot-to-module was unlikely to come to fruition, also reverting to semi-only play. However, while these scenarios may seem somewhat earthshattering to many, it is worth remembering that these three non-China-headquartered companies supply less than 5% of solar end-market supply today.

This exercise also opens the question of new polysilicon capacity coming to fruition in the Middle East and Africa region (MEA), and whether production here will allow sector growth to be maintained from 2027 onwards. However, this may not seem as clear cut as it seems.

The MEA polysilicon aspirations may not be what they seem at first glance, like much of the ingot, wafer, cell and module plans that have been announced recently in this region.

Behind most (if not all) of the projects (announced, under construction or operational) is money from China, with a key driver ultimately being to supply modules to the U.S. market; not regionally funded capacity build-outs to serve domestic markets and help countries there increase solar deployment rates. In this respect, there is clearly risk from U.S. policy decision making.

Despite these uncertainties, it could be 2027 (or 2028) that marks the start of new polysilicon capacity being required to contribute to overall production levels. If there is sufficient capacity to serve end-market growth through 2027 (helped if growth rates are not at the high end of forecasts), then 2028 capacity additions would require investments to start next year, in 2026. This could well end up being fortuitous in timing, with 2026 likely to see the first green shoots emerge in PV capex, if cost control measures over the next 6 months pay dividends.

However, like all forecasts in the PV industry, it is often the ‘unknown unknowns’ that have the largest impact, for example: plant outages owing to fires or natural disasters, new trade regulations that create localised manufacturing and export restrictions, global conflicts or new geopolitical alliances, or an unexpected short-term boost for renewables arising from a change in energy supply sentiment.

Scrutiny on global supply-chain traceability is not going away

Regardless of which permutations outlined above come to fruition, the need to understand polysilicon producers’ upstream suppliers and downstream customers is only going to gain traction.

Since the 2021 Sheffield Hallam report, various third parties have sought to create working ‘templates’ to address this issue. However, all have been either country/region specific (such as in the U.S. and Europe), or have excluded (not included) active participation of Chinese companies.

Also, the focus of these has often been overly biased to module supply (going backwards or upstream on well-defined value-chain supply arrangements), rather than starting upstream (say at the polysilicon level) and following polysilicon production down through ingot customers and their channels at the wafer and cell stages, to ultimately arrive at module offerings to end market segments and users.

A global solution is surely needed here and one that has China at the centre, not brought in to satisfy the needs of the Western world. Whether this is doable or not is another question, but one can only strive for such clarity in solar PV production and supply-chain traceability. Having this in place as the sector moves to annual muti-terawatt productivity levels would be a huge step forward for every stakeholder in the industry at this time.