The solar photovoltaic (PV) manufacturing sector entered 2025 in desperate need of a success story, with a decimated Chinese sector, a fragile U.S. landscape, and a confused European investment climate.

If there was ever a year for a sleeping giant to emerge on the scene and give hope to the global PV manufacturing community, it was 2025.

And for those inclined to champion an underdog – often overlooked as a potential manufacturing powerhouse – 2025 ended up a year with much to celebrate.

It will be remembered as the year that India finally hit the stage as a PV manufacturing country of relevance, representing the one big success story in an otherwise bleak and depressing year for PV manufacturing globally.

And much of this credit goes to a select group of about 20 domestic-owned Indian crystalline-silicon (c-Si) module producers, and one foreign manufacturer (First Solar).

Collectively, this group of companies is now accounting for more than 95% of PV modules being deployed in India; potentially, the first box needing to be ticked by the sector before turning seriously to other parts of the upstream manufacturing value-chain.

This article focuses on two important leading metrics for this dominant top 20 grouping (adding in First Solar from now on here, making a total of 21 in fact, and referred to below in ‘white ball’ lingo as ‘T20’).

The two leading metrics referred to above are production output and capital expenditure (or capex); parameters that are often overlooked, compared to other somewhat ‘meaningless-metrics’ that typically attract headline viewing figures (such as country-wide government capacity numbers, grand plans from entities that never come to fruition, or aspirational long-term renewables deployment targets).

Factoring in the module shipment volumes from each of the T20 companies (specifically what portion of shipped product is exported) and comparing to imported modules to India (mainly from China and Southeast Asia) allows an accurate assessment of the domestic production-versus-consumption ratio to be monitored.

Domestic cell production and imported cell volumes to India during 2025 then provide the final data needed to triangulate and forecast final India module production levels for the year.

While timelines associated with imports/exports, production/shipment, upstream/downstream inventory (or tactical stockpiling) and installation grid-connection/site-completion are always staggered (in any market globally), focusing on domestic module production for domestic consumption from a key group – that accounts for >90% of the market today – is probably the most accurate way to understand what is really happening with PV manufacturing in India today in real time.

This article also looks more broadly at some of the key issues routinely being discussed and questioned in recent times, regarding PV manufacturing in India.

Some of these issues are new ones – in particular, investments from pure-play renewable independent power producers (IPPs) into module manufacturing as a means of securing in-house component supply and potentially generating cash from third-party module sales to fund new upfront project costs.

However, many of the issues have been seen before in the PV industry over the past 20 years or so, and are not new: a misunderstanding of what ‘capacity’ means in the solar industry; the challenges in moving from module-assembly to cell-fabrication; the risks in building factories that end up taking years to complete, not months; an over-dependence on foreign countries for production equipment and technology know-how; and no clear plan to compete globally in a worse-case scenario arising from domestic policy reversals or external trade factors, or a gradual erosion in production gross margins (or simply pricing heading south).

The complete discussion of all these points will come to light over two separate articles (Part One here, specific to modules). Factoring in cell production and associated capex dynamics will be the subject of a follow-on article (Part Two). Remember that ‘technology’ is not a module dynamic – it is cell specific; a salient point yet to be fully absorbed by many in India today. Again – more on this in Part Two.

Before diving into the collective data from the T20 group of module suppliers in India today, let’s remember that what has been achieved within India for PV manufacturing in the past five years is nothing short of a miracle.

A miracle that I never saw coming some 20 years ago when I set out analysing global PV manufacturing and benchmarking the competitive strategies of technology-based companies in the sector.

Previous manufacturing initiatives ended up in tears

My first business trip to visit solar manufacturers in India was more than 15 years ago, when there was a real impetus in the country to create a domestic solar manufacturing industry (especially for c-Si cells and thin-film panels).

Having just visited the leading PV manufacturers in Japan, South Korea, Taiwan, China, Europe and in the U.S., India was the final port of call back in 2009.

If nothing else, perhaps just finding out Tata’s intentions in Bangalore for its joint venture partner’s (BP Solar) laser-grooved buried contact (LGBC) cell architecture (licensed from the University of New South Wales) would justify my expenses for the business trip. LGBC cells were cutting edge back in 2009, and Tata’s association with BP Solar was potentially India’s ticket into advanced c-Si cell production.

My trip at the time overlapped with investments by prominent players in the India PV sector to put the country on the solar manufacturing landscape, hoping to compete with established cell producers in Japan, Taiwan, and Europe.

Among the factory visits during this trip included the new multi c-Si cell line at Indosolar in Greater Noida with a state-of-the-art turn-key line from German tool maker Schmid.

Indosolar was preparing for an initial public offering (IPO) placement, championed by owners that had prospered earlier in the manufacturing of halogen lamps in India. (Notably, this fab was recently acquired by the leading T20 player today, Waaree, as part of its 2025 module capacity expansion plans.)

Everywhere, there was also a feeling of ‘newness’ during the trip back in 2009.

Travelling at the time from Delhi to the newly opened Hyderabad airport in Shamshabad conveniently transported me to Solar Semiconductor’s factory at the equally-newly-built ‘Fab City’ complex.

Again, equipped with production equipment from Germany, Solar Semiconductor epitomised the feeling of discovery then in India and the excitement and pride of a ‘Fab’ even coming to fruition in the country.

Sadly, the company failed to evolve much beyond the equipment ramp-up phase. Years later, the facility was acquired by another T20 player in the India PV sector today, Premier Energies.

However, the highlight of the trip was not related to c-Si manufacturing but thin-film solar. A stones-throw from Indosolar in Greater Noida, Moser Baer had truly hit the global solar stage.

Moser had just become Applied Materials’ first customer for its major push into the PV sector as an equipment provider – the supply of turn-key amorphous-silicon (a-Si) production lines (coming with a not inconsiderate price tag in the range of US$100 million).

Moser was bullish in its solar plans; investments up to US$5 billion were slated for new manufacturing facilities in Tamil Nadu, Telangana and Andhra Pradesh, in addition to expansions at Greater Noida (Uttar Pradesh).

Regarding the initial thin-film tool order, press releases were in abundance from Santa Clara (Applied Materials) lauding the first-mover status of Moser Baer at the time; Moser not alone globally in being smitten by the prospect of a potential new revenue stream from a-Si thin-film solar panels. In Moser’s case, this was intended to address declining sales and growing losses from its core CD/DVD data-storage manufacturing activities.

However – completing what would ultimately become a trio of subsequently-insolvent company factory visits from my trip more than 15 years ago – Moser Baer joined the global contingent of failed a-Si thin-film aspirants.

At the time, India had somewhat gambled on a PV manufacturing entrance, strongly influenced by Western equipment suppliers seeking a new geography to capitalize on. And within no time at all, Chinese solar companies had mobilized effectively to own the next decade of solar manufacturing.

And not even Taiwan could compete then with China on solar manufacturing, crushed by its dominant neighbour when Taiwan solar cells were no longer needed in China; what chance for any other country, especially India back then?

Fast-forward to today, more than 15 years after Moser Baer’s decision to invest in thin-film (coupled with government support in the technology), India is now home to one of the few thin-film fabs in operation in the PV industry – First Solar’s CdTe factory in Tamil Nadu. Poetic justice perhaps.

Investor confidence in India PV manufacturing in stark contrast to rest-of-the-world

Factors behind the uptick in PV manufacturing investments within India over the past few years are well known: heavy import duties (the basic custom duty, or BCD) on cells and modules; an attractive Production-Linked Incentive (PLI) scheme for domestic manufacturing; rules based on inclusion within the Approved List of Models and Manufacturers (ALMM); and mandatory domestic component usage from Central Public Sector Undertakings (CPSUs).

However, sitting alongside these policy-driven initiatives are factors that have created (until now) an investment-friendly landscape for PV manufacturing capex that has allowed about two dozen notable new entrants to the sector in the past few years, sometimes with no prior experience in manufacturing of any type.

This bullish investment climate for PV manufacturing in India today has been supported (again, until now!) by an almost risk-averse attitude to long-term government support for solar as a technology (both manufacturing and domestic deployment levels), maintaining selling prices that are 50-100% above global averages and having companies running fabs (almost from day one) with double-digit operating margins and negligible liquidity or debt concerns.

Providing a further level of confidence in the sector arises from the active participation of some of the highest-valued conglomerates in the world – Reliance Industries, Adani Group and Tata Group – through subsidiary operations or in-house business units. As a rubber-stamp of approval, validation stakes don’t come any higher.

Now add in recent India PV entity Draft Red Herring Prospectuses (DRHPs), IPO placements, enthusiastic ratings reports from the various agencies assigning creditworthiness to sector participants, and exuberant listed-entity quarterly calls with a new ‘batch’ of solar equity analysts; each appearing to fully support a widespread feeling of optimism for solar manufacturing expansions and profitable operations.

It sounds too good to be true.

Indeed, this landscape in India could not be more different to the rest of the world as it pertains to solar PV manufacturing and new capex allocations.

Currently, India is an outlier, coming at a time when China is recovering slowly from a dramatic manufacturing downturn that has decimated earnings and cash reserves accumulated during the past decade.

Moreover, contrast the support for solar manufacturing within India to the current climate in the U.S., where risk and uncertainty are rife and the strategy for PV manufacturing is hugely fragmented and often beset with legal tactics to thwart competitive market-share concerns at the company, technology and foreign-ownership level.

Ask yourself: what gives India a monopoly on solar manufacturing and policy wisdom?

And remember: module production has the lowest technology barrier-to-entry as the final component assembly part of an entire silicon-based value-chain.

How many GW-scale module producers are needed?

It is amazing to think there could be a problem in having too many GW-scale PV module producers in India. Ask ten people the question in the sub-heading above, and you may get ten different answers today.

CEOs of existing, leading (say top five by volume) module producers in India talk about the ‘need’ to have a few dominant players, as they would.

New entrants talk about the ‘market opportunity’ for expansion and why they are needed to ‘help’ in hitting aspirational government targets for solar by 2030. As they also would.

And third-party observers routinely default to the word ‘consolidation’, without any evidence to support the prognosis and unaware that this has been the most misused and erroneous term in PV manufacturing over the past few decades.

Before I give my own take on the question, let’s look at some of the issues in play today with a few dozen companies seeking to make PV modules in India at the GW-plus level.

In terms of the cumulative impact of this (the overall numbers), it is a topic that is (as expected) being discussed, often by market research firms (many not active in the India PV sector until recent times) or global news agencies (that often favour alarmist headlines).

As I will explain in more detail shortly, simply grabbing a government statistic or two and proclaiming that serious problems are just around the corner can often be considered as naïve and short-sighted. Especially in the solar industry.

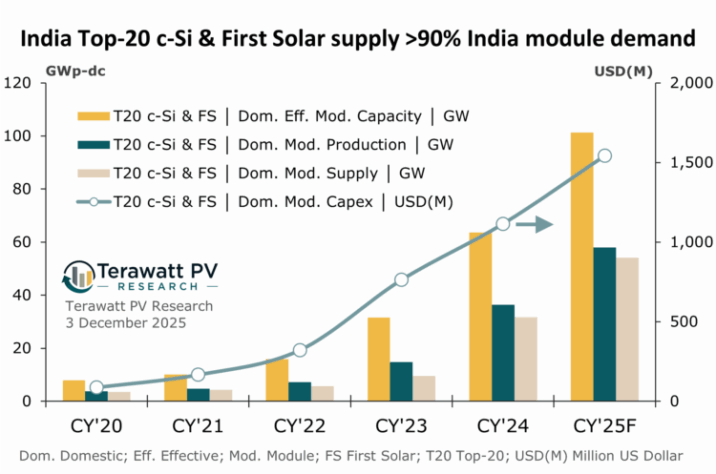

Before returning to the T20 analysis now to illustrate this, it is worth pointing out that all years cited in this article and accompanying graphics refer to calendar year periods, not fiscal years; for example, CY’20 means the 12-month period for the calendar year, 1 January 2020 to 31 December 2020, etc.

Until 2021, India had never had a single company producing more than 1 GW of modules in a single year. Few companies – if any – even had the nameplate or effective capacity levels (or order books) to threaten this landmark achievement. And a good deal of the early players in the sector counted cumulative decade-long production levels in the tens of megawatts range.

Amazingly, fast-forward to 2025 when there is expected to be 18 companies each producing more than 1 GW of modules during CY’25, and with 2026 possibly seeing the GW-group membership list expand to circa. 25-30 companies.

Furthermore, about a dozen companies in India will close out 2025 with annual module production volumes in excess of 2 GW – more unchartered territory indeed.

Back to the question in the subheading above – how many GW-scale producers are needed? Well, I would suggest that this question depends on what the end goals for the likes of Reliance, Adani and Tata are. Or for many of the other module producers, how much being on the global stage matters.

There are many reasons why having a larger number of mid-sized module manufacturers is preferable to having a few large entities calling the shots.

Over-dependence on a handful of companies ultimately puts the fate of a sector in the hands of a few. Having too much capacity at the company level can also be a problem in a downturn; rather than spreading out capacity allocations across a wider range of stakeholders (and geographies).

Diversifying the supplier pool is also much better than a situation where a few conglomerates are left to operate somewhat in isolation from the others, detached at times from the grass roots of an industry, and ultimately entwined themselves in government policy lobbying and decision-making regarding energy supply and infrastructure spending.

Having module suppliers whose business models are differentiated could also be a massive plus; in particular, when order books are curtailed or margins are compressed. Having secondary revenue streams is essential for PV manufacturers.

Currently, the stakeholders in PV module assembly in India represent a more diverse range of entities than seen before in the history of PV manufacturing, including:

Pure-play module assemblers; PV-specific module and upstream wafer/cell proponents; module suppliers with existing or newly-financed materials supply business units (encapsulants, backsheets, glass and frames); recently listed, public-traded, mid-size companies with strong participation now in energy storage and green hydrogen; IPPs that have moved into module manufacturing to meet in-house module supply requirements; and of course, the participation of the conglomerate trio of Reliance, Tata and Adani (alone a differentiator that trumps all-of-the-above).

Potentially, this blend of participants could create a more dynamic and market responsive PV manufacturing sector than the solar industry globally has witnessed in the past. Furthermore, aside from First Solar, all companies are Indian-owned and operate with a more holistic, mutually respectful and collaborative ethos than in evidence in China and the U.S. today. Furthermore, India is not a market plagued by short-term opportunistic plays by overseas entities looking for a quick buck.

A few years back, I discussed through a series of online feature articles how the U.S. could develop its domestic manufacturing industry. Having a spread of module assemblers directly connected to the needs of the end-market was one of themes that appeared to be attractive then.

However, this was not the conclusion for building out a robust cell manufacturing landscape; something I will return to in Part Two of this India manufacturing series of articles.

Why is ‘capacity’ always the most misunderstood word in the solar industry?

Analysing the operational performance of the India PV manufacturing landscape in 2025 is very different to 15 years ago. Different to 10 years ago for sure. But not that different from 5 years ago – just with a more players.

To get the needed perspective today with still one month left in CY’25 – as opposed to waiting for another 4-5 months and reporting on CY’25 in hindsight – a select group of 20 c-Si module producers in India (and First Solar) gives that 90%-plus threshold that is more than good enough to call out the major issues of the year.

It turns out that the ‘threshold’ for inclusion (for the India T20) in 2025 is to have produced more than 500 MW in the year. Again, who would have thought back in just 2020 that being a 100-400 MW annual module producer would have been of secondary importance to India’s overall annual production output of PV modules?

The vertical bars in the graph above refer to the cumulative annual module capacity, production and domestic module supply of the T20 companies.

The capacity bars (in orange) represent the cumulative effective capacity of the T20 companies summed over available quarterly capacity volumes. Effective, not nameplate capacity, should always be used in market research. In the case of modules, this effective capacity should also be re-evaluated based on cell technology, tool throughput and yield improvements.

The CY’25 figure of the T20 group at circa. 100 GW may surprise and concern many, but the trajectory of effective capacity and production shown in the graph above does not strike me as anything out of the ordinary.

The ALMM (List I) provides a glimpse into country-specific module manufacturing capacity, the details of which are unparalleled elsewhere globally (today and at any time in the past): but the list does need to be interpreted with caution.

About half of the circa. 80-100 companies in the ALMM do not contribute in any meaningful way to market fundamentals, with some for example mainly undertaking OEM work on demand.

Cited capacity numbers are at times on the high side for some companies but there are plenty of examples where stated factory capacities are lower than effective rates due to higher throughput equipment having been installed, adjustments made to account for the use of higher efficiency cells being used today, or simply a lag in registering capacity additions.

However, the overall capacity figures turn out to be a very good approximation of the effective capacity available from the relevant players in the near to mid-term (a pool of about 40 module manufacturers in India today).

The problem lies in interpreting the effective capacity in terms of production output and this is where most of the confusion arises in the mainstream press. This is not a new dilemma in the solar industry. It is perhaps the most common misunderstanding I have come across in PV market research in the past few decades.

An extreme example of this misrepresentation of ‘capacity’ is seen routinely in company-specific documentation (sales and marketing output, and even in DRHPs or quarterly filings) when Indian module manufacturers cite their ‘market-share’ based on their own planned capacity (in the future) relative to the overall planned capacity of the sector. This is the first time I have come across this, and it beggars belief that no-one is calling out these market-share claims as highly erroneous. Market-share should be based on actual production, shipments or revenues; not aspirational ‘capacity’ metrics.

60-70% utilization rates are good!

In a rapidly growing manufacturing environment – such is the case for module assembly in India since CY’23 in particular – it would be expected that actual production trends at about 50-60% of effective capacity installed.

During the period CY’20 to CY’23, utilization rates (actual production to effective capacity) for the T20 were 46-47% every year, seeing a step-wise uptick to 57% for both CY’24 and CY’25.

Even if capacity additions were halted tomorrow, one should not expect this percentage to increase much beyond the 65-70% level, given demand seasonality, fiscal year-end surges in supply, line maintenance and upgrades, and order-book variations over the year. Or simply based on the fact that some factories are never intended to be run in anger at any given time.

Even the most efficient Chinese module suppliers run at 80-90% utilization rates at the best of times. Many others in China typically output at the 50-60% level. First Solar is the only PV manufacturer ever to have utilization rates from its factories in the 90-95% level over a sustained period.

But scrutiny on the cumulative effective capacity numbers in India will inevitably become an issue, and this will likely happen within the next couple of years, prompting adjustment phases, not cataclysmic self-implosion (as some commentators have alluded to of recent).

Exporting modules from India; essential, optional or out-of-desperation?

Installed capacity by many of the companies currently ranked in the 20-40 positions in terms of production is set to grow next year (many ramping up 1-2 GW plants today). Coupled with the build-out scheduled from the T20 companies, this is inevitably going to lead to changes in market dynamics in 2026. Domestic demand (anywhere globally in the renewables sector) can only sustain a certain degree of elasticity.

This limitation in end-market elasticity (how much a market can grow through an uptick in supply) is typically determined for solar by how fast utility-scale providers can fast-track build-out phases. This has been seen many times before in the sector; where planning, financing and grid-availability are often the gating factors in accelerating end-market growth.

A similar situation was seen a few years ago in Europe which acted as the catalyst for a rapid module pricing decline, which continues today. There is every reason to suggest that module pricing will be affected similarly in India under this scenario.

Normally, one would expect manufacturers to pivot to export sales over domestic business when order pipelines begin to contract. However, India has created a solar landscape that essentially supports domestic deployment only (from a profitability standpoint).

Taking the U.S. market out of the equation today for exports, the solar ‘world’ outside India is typically buying modules made in China and sold (DDP) below 10c/W (USD).

Therefore, one would expect pragmatism to kick in, regarding some of the capacity expansion claims or plans; thereby avoiding some of the scaremongering headlines that have been broadcast in recent months by third-party observers of the India PV sector.

For example, module capacity figures (again often erroneously converted directly into production output capability) as high as 300 GW have been banded in recent weeks. And there is no shortage of spreadsheet summations being made simply adding up ‘plans’ without stopping to consider that ‘plans’ are simply that – and companies change plans based on market conditions.

Domestic order books for many of India’s module producers (perhaps excluding the likes of Reliance) will adjust according to order books. The idea that a company that has glibly announced a five-year expansion plan will simply enact on this no-matter-what is not how the world works.

Companies will adjust follow-on phases of investment if initial line build-outs are not operating at acceptable utilization rates or there is a lack of confidence that an order uptick will unfold to justify additional capex for manufacturing capacity. This is not pragmatism confined to solar or India!

In recent years, India’s PV manufacturing segment has exhibited fiscal prudence levels that are almost unprecedented, compared to much of the PV manufacturing community elsewhere; keeping long-term debt under control, ensuring cash-flow is safely in the black, and releasing new capital expenditure in phases.

Contrast this will some of the localized boom-and-bust periods of Chinese new entrants to wafer, cell and module manufacturing in recent years. Companies new to the industry, building 10-20 GW fabs in blind faith that orders will arrive on tap when a factory happens to be completed.

What is more likely to happen with many (in India) is a pause on module plans and perhaps a focus on bringing cell capacity to levels that match module capacity levels installed up to the end of 2026.

Returning to the graphic for the T20 again.

Now that the relationship between the effective capacity (orange vertical bars) and the actual module production (blue bars) has been explained, the next part of the analysis focuses on how much of this domestic module production remains in the country and how much is exported.

This can be seen over the years on the graph by the delta in heights between the blue bars and the light-brown bars (labelled Domestic Module Supply); the difference being what is exported.

Having export sales has been an on/off activity for the Indian PV sector over the past few decades. During Europe’s feed-in-tariff phase 15-20 years ago, Tata and Vikram were the main beneficiaries. By the time new entrants such as Waaree appeared on the scene, Europe had moved into a ‘post-subsidy’ era.

This led to a period of somewhat enforced isolation from the world for the handful of Indian module suppliers that were weighing up the return-on-investment in having overseas sales and marketing activities.

Vikram was the exception at this point, setting up U.S. operations that saw modest returns. By the time the U.S. got serious about closing down supply channels from China, Taiwan and Southeast Asia, Vikram was joined by Waaree and Adani, as a fortuitous window of opportunity arose for modules to ship from India to the U.S. without any import duties.

Subsequently, it seemed that almost every other Indian module supplier was setting out plans to be a player in the U.S., where landed module prices in the range 25-30c/W were on offer. Indeed, as production-based incentives were introduced in the U.S., these fleeting U.S. export aspirations morphed into highly ambitious plans to set up overseas module assembly operations.

India was not alone in this wave of investment planning euphoria for the U.S. market and, after all the noise had largely dissipated, only one Indian module supplier had enacted on its plans, Waaree (benefiting from early-mover IPO listing status). An achievement of sorts for Waaree, it remains to be seen if loss-making activities from its U.S. operations in recent times can be reversed.

Today, being a preferred module supplier for U.S. buyers has a greater level of scrutiny than anywhere else globally, almost independent of whether modules are being imported (safely through customs) or made domestically.

It is no longer simply a case of having dedicated sales and marketing operations in the U.S., but having security of supply-channels, transparency in corporate operations and the engagement of legal counsel (in the U.S., likely DC-based) to advise correctly on increasingly complex policy implications. For most Indian module suppliers today, this effectively removes the U.S. as a viable overseas market channel for sales. And there is the issue of increasing barriers being placed on exports from India to the U.S. in general.

Capex is a cyclic phenomenon

The final metric of interest shown in the graph above relates to module-specific capex in India from the T20.

This is shown by the line in the graph (plotted to the right on the secondary axis). Conversion is done to U.S. dollars on a quarterly basis. A pro-rated allocation for First Solar’s total Tamil Nadu capex is done to extract a like-for-like ‘module’ only allocation for the company, allowing the total capex from the T20 group to reflect module-only factory spending levels in India.

Capex has always been one of the most important leading indicators in the PV industry. Today is no different; in particular, as it relates to the three different geographic zones of manufacturing in play (China, India and the U.S.); areas that are currently out-of-synch in terms of capex cyclicity. China in recession, India enjoying an upturn phase, and the U.S. betwixt and between.

The upward tick in module specific PV capex in India since 2023 is in stark contrast to China, where the manufacturing sector is deep into a 2-3 year downturn cycle that has seen capex levels decline markedly in 2024 and 2025.

While opportunities for module capex in China are confined largely to maintenance-only spending, the circa. USD$1.5 billion committed within India for module expansions in 2025 by the T20 alone goes a long way to explaining why so many Chinese PV equipment suppliers are prioritising India from a marcoms perspective.

It is likely that more new module factories will be built in India during 2025 than the rest of the world combined. How incredible is that?

However, analysing PV capex goes beyond just adding up companies’ spending contributions through the value-chain. It allows technology trends to be understood in great detail, and a full discussion on this fascinating dynamic in India falls not with the module assembly additions, but cell line additions.

Again, expect a follow-up to this article soon that looks at the benefits and threats arising from the spending trends across the emerging India cell production landscape today. And how this will bring to the fore the importance of having country-specific technology leadership credentials.

As night follows day, PV manufacturing capex in India will exhibit a cyclic spending profile. It is impossible to get forward-looking capex allocations (from a whole sector perspective) 100% correct and aligned perfectly with the progress of downstream channels (customer base). Spending tends to be either too-high or too-low at any given time. Major problems only arise when spending is first, too high, and then, not corrected.

PV capex allocations in India are not simply decoupled from global PV capex cycles, module and cell in India are also out of phase. It is entirely feasible that cell capex peaks at the same time as module capex moves into a downturn phase.

It is too early to call how this now. A clearer picture will emerge by the middle of 2026. But worrying about periods of over-spending is infinitely better than no spending at all.

The bottom line is that PV manufacturing capex – in any form and at any time – for new cell and module capacity in India still needs to be celebrated, not chastised.

For PV manufacturing capex in India in 2025 (and to a lesser extent in 2023 and 2024) has finally propelled the country into box office status as a potential manufacturing powerhouse.

Decisions made going forward – in particular, regarding cell production and technology evolution – will ultimately determine whether India’s solar PV manufacturing sector reaches the end of the decade as a global game-changer or just the end-result of an insular protectionist policy regime that ended up being a copy-and-paste of Chinese state-of-the-art production line availability.