This article is the second of two based on the recent presentations I delivered at the PV ModuleTech USA 2025 event in Napa, California.

In the previous article – China’s 2025 supply-chain reset a bigger threat to US manufacturing aspirations than policy change – I highlighted the cost reduction strategies being prioritised in China this year, and the far-reaching impact this will have on the global sector from 2026 (and throughout the terawatt transition phase of the industry).

This article focuses on the other key theme I addressed in Napa; PV supply-chain traceability.

Everyone wants transparent and simple supply-chains

For more than 20 years, understanding who is making what type of products and where – through the entire PV manufacturing supply-chain and down to equipment and materials suppliers – has been a key priority.

In part, this provided checks to guide the overall production landscape in the industry: it offered a means to assess technology segmentation and roadmaps; and it was critical to size and forecast capital equipment spending and direct material consumption.

Qualitatively, I always assumed that companies with the greatest level of in-house vertical integration would be able to retain the highest degree of quality control of components (ingots, wafers and cells), used for their own module assembly lines.

However, in practice, the industry has evolved over the past 20-30 years in a more fragmented way, with only a handful of silicon-based manufacturers coming anywhere close to having most of their module-based upstream components produced in-house.

As I explain later in the article, this flexible type of manufacturing model (fab-lite analogous or even fabless) has proved successful for many companies over the years and has a host of advantages.

However, when downstream module buyers, government agencies and trade-based organisations start looking into supply-chains and traceability, the companies that have benefited from this diversified model appear to want to distance themselves from its reality.

Indeed – regardless of Xinjiang or FEOC (foreign entity of concern) related questions even being in the mix – there is definitely a strong desire by module suppliers to portray more simplified supply-chain operations; ones that can be audited with certainty (or in effect, be traceable in origin).

Fortunately for all concerned, module-buying and traceability is certainly being taken more seriously today compared to any time in the past (albeit not necessarily to ensure product quality is optimized).

Like opening a can-of-worms, module purchasing teams must yearn for the days in which price and delivery-time were the two key questions to be answered by module companies.

Sellers and buyers alike would love the industry to have a simple solution to traceability, and one that didn’t seem to change each month.

However, this desire to find neat single-supplier channels – often as the main objective of due-diligence and outsourced factory auditing – does not address the reality of the sector, and how it operates in practice.

Perhaps, if the starting point was more pragmatic, there would be a greater understanding of the key issues to address with regards traceability maps being advocated on the supply side; and then which of these module buyers were willing to accept at any given time.

Either way, it all comes back to knowing who produced what and where, through the value-chain.

In this respect, the starting point is to capture how supply-chains operate for any given module supplier, with the different options being employed by them in-house and outsourced to third parties. This seems like the only way to have transparency: not to present one simplified model that is one of many in operation.

No right-or-wrong in having multiple supplier options

As highlighted above, having multiple supplier options is good business practice and allows for a strategy that can avoid having underutilised assets at some point in the future.

Take the example of an integrated cell and module producer, of which there are a few dozen in the sector today. It makes little sense to have a single, or dominant, wafer supplier for in-house cell production. Looking at the options for wafer supply today, this could end up being a competitor (that is selling wafers externally and consuming internally) or – in the case of a pure-play wafer producer – a company whose ongoing operations could be at risk if cashflow and debt become trading impediments.

Furthermore, one cannot foresee what factors could arise with location-of-manufacturing in the future, as evidenced by Xinjiang and related FEOC questions, not to mention import restrictions on Southeast Asian countries. For example, imagine, say, if somewhere like Inner Mongolia was put in the spotlight today by certain Western governments, in the same way as Xinjiang a few years ago? How would this disrupt upstream supply-chains?

In addition, cell producers being able to tap the spot market for wafer supply in an opportunistic manner can be highly beneficial, especially during times when wafer pricing is depressed, as happens routinely during downturn cycles in the industry.

Therefore, having multiple options for wafer supply is probably more of a necessity than a luxury.

One can now apply this same logic to pure-play module suppliers that need to buy from third-party cell producers, and to the wafer producers themselves. While the wafer segment is typically ingot/wafer matched to a close degree – and ingot trading is still undertaken routinely in China today – here we are looking primarily at the ingot/wafer producers buying in polysilicon (often under a mix of short and long-term contracts).

The argument for having multiple polysilicon suppliers is even more compelling than for cell producers having to buy in wafers. This is chiefly because of the Xinjiang ‘history’, and the fact that outages at polysilicon plants happen and the risk here needs to be factored in.

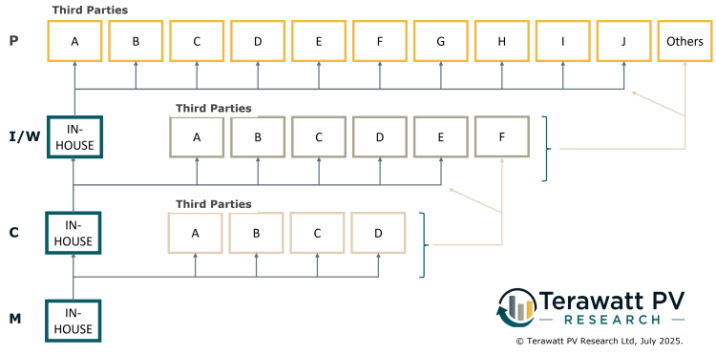

Now let’s move to the figure above. This was prepared specifically for the Napa session and involved a few hours scanning annual reports of about a dozen listed companies going back five years.

Direct/secondary supply-chains a near catch-all

In the days before the talk in Napa, I decided to dissect the supply-chain for one of the top five global module suppliers to the industry in recent years, scanning though audited supplier/customer documentation going back to 2020, while factoring in how much ingot/wafer and cell production had been done in-house (compared to third-party sourced) over the past five years.

The module supplier in question can remain anonymous for now. I suspect any of the top five Chinese PV module suppliers globally would have had similar flow-charts created. Anyhow, the goal was not to ‘name names’: rather, to show how supply-chains work in the PV industry.

In the figure above P, I/W, C and M refer to the polysilicon, ingot/wafer, cell and module stages of the c-Si value-chain.

Starting from the bottom of the figure, cell supply to in-house module production (for the chosen module supplier) has been coming from a mix of in-house cell production and from third parties. Over the past five years, there have been four key cell suppliers. Therefore, before we go any further upstream, supply-chains are already beginning to bifurcate.

From a number’s standpoint, somewhere in the region of 30-40% of cells were outsourced over this five-year period (for the module supplier in question).

Moving on upwards from cells, wafer supply for cell production is again a blend of in-house wafer supply and wafers from third parties. Compared to cell-supply-to-module-production above, a greater percentage of wafers was from third party sourcing. Indeed, this required five main wafers suppliers over this period.

Now one needs to consider also wafer supply channels to the third-party cell sources used. This is almost certain to encompass other wafer producers; possibly all other remaining volume suppliers (as the industry pool here is typically only about 10-15 in number).

Finally, from ingot back to polysilicon, probably the key finding was that ten different polysilicon suppliers had been used (over a five-year period) for the ingot/wafer production stage, by this leading module supplier; basically, almost every polysilicon supplier in the industry.

Earlier in this article, I touched on why polysilicon diversification has been essential for companies active on the global stage (and especially those that have been shipping modules for the U.S. market). Therefore, it is not a surprise that a leading global module supplier over the past five years (with in-house ingot/wafer production) has been supplied by most of the polysilicon suppliers globally.

When I delivered the talk containing this slide, I pointed out that this direct and secondary supply-chain analysis – that ultimately links one module supplier with the 25-30 entities that make more than 90% of all upstream c-Si components today – was one of the reasons so many companies in China had been successful over the past decade.

In fact, until only recently, having such a flexible in-house/outsourcing supply-chain was considered by many (including most of the equity analysts of the past 20 years) to be more of a positive than a negative.

Remember that the figure was from a quick scan over five years. At any given time, the number of polysilicon suppliers is probably about half of that shown, but wafer and cell numbers are broadly consistent with what is on the figure.

Indeed, the supply-chain options can reduce in number quickly if in-house wafer and cell production quotas are increased (possibly just needing a couple of third-party options for cells and wafers). In some respects, this probably offers the best chances to simplify the sector supply-chain variances, and this could end up being a winning outcome for many in the future.

The burning question though is really: what will a multi-terawatt production landscape look like? Different or more of the same?