Two weeks ago, I delivered my first PV conference presentations since going ‘solo’ at the end of May 2025, at the PV ModuleTech USA 2025 event in Napa, California.

For the opening talk of the conference on Tuesday 17 June, I focused on what I considered to be the major themes impacting global PV manufacturing today. I thought this may offer the audience (primarily focused quite rightly on U.S. solar PV issues) some insights into what was happening in Asia (especially China) this year.

The second talk, on Wednesday 18 June, was part of a two-hour panel session where the slides were to provide context for supply-chain traceability.

This article is the first of two to feature on the Terawatt PV Research portal, looking at the specific themes covered during these talks.

Cost reduction works if supply-chains are willing partners

Outside China, it seems these days that the world has become preoccupied with the reining in of U.S. solar incentives that had been a key part of the industry’s profitable downstream sector in recent years.

However, what is happening this year in China will have a greater impact for the global sector – including the U.S. – from 2026 onwards: specifically, the fact that the domestic Chinese sector is adjusting to the module pricing norms that set in about 12 months ago, and the key players are focusing on the only game in town now, cost reduction.

2025 is one of the most important years for the Chinese solar sector since its meteoric rise in the past 15 years; a year in which cost reduction efforts need to be implemented across the board, more so than required in the past (including the first manufacturing downturn in 2012).

The goal is to get to a point where the cost-of-goods-sold (COGS) for modules is comfortably trending at 10-15 percent (plus/minus 5 percent variable) below module sales prices. For the past 12 months – since the effects of the manufacturing downturn took grip – costs have been higher than sales.

To reach this goal, the entire Chinese sector needs to be in alignment. This starts with polysilicon suppliers accepting that for the foreseeable future, prices will not deviate significantly from the circa. 35 RMB/kg level. While this is largely outside the control of the major module suppliers, they do have the ability to work on other direct materials costs, in particular glass, films/backsheets, frames (all at the module level), silver usage (the cell level) and other costs such as diamond wires for slicing wafers.

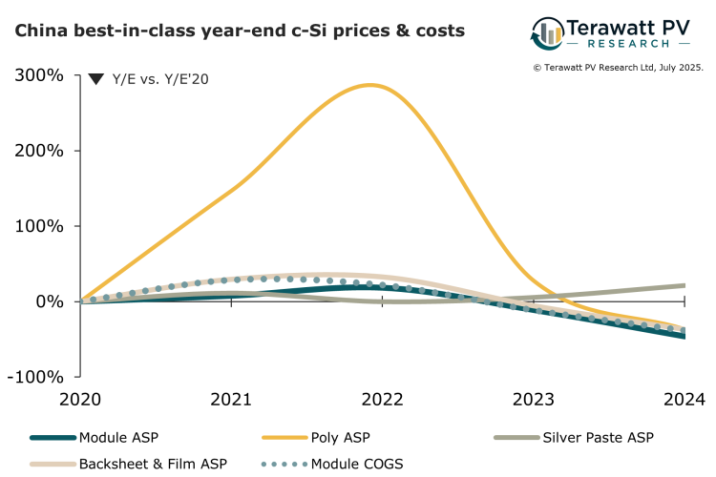

To understand how pricing through the value-chain has trended in the past few years, I have done a quick back-of-the-envelope analysis from the latest cost data from a sub-group of 15 suppliers and producers in China today. The result of this analysis is shown in the graph attached to the article and discussed in the section below.

Key takeaways from the graph

The graph shown considers five metrics (module average sales price, or ASP, through to module COGS) and how much each of these changed at the end of each calendar year from 2021 to 2024, compared to their values at the end of 2020 (the starting point).

The reason for choosing the year-end (Y/E) period from 2020 to 2024 is because the sector effectively went through the tail-end of an upturn and the onset of a downturn during this time.

Put another way; at Y/E’20, most of the supply-chain in China was in a somewhat comfortable position with respect to gross and operating margins. Debt levels were under control and capacity expansions were being funded from a mixture of cash, debt, and new share placements.

The graph clearly shows the disproportionate spike in the price of polysilicon, but an equally steep decline to a position at the start of 2025 (and with no signs of reversal by mid-year) where polysilicon has taken the same overall hit at modules over the 5-year phase shown.

The sharp fall in prices across the value-chain as a whole can be seen when comparing the Y/E’23 and Y/E’24 changes, with the exception of silver paste that is one of the few direct materials that is close to the pricing of silver power itself (which is ultimately fixed relative to a precious metal price index).

While not directly visible on the graph, the module COGS delta at Y/E’24 (and through 2025 so far) has not fallen as much as the equivalent module ASP. Essentially, this confirms the work-in-progress on the cost reduction activities in China. I expect this has about another 9-12 months of efforts left.

Module cost reduction is not as simple as lowering the purchasing costs from 3-4 materials suppliers. Rather, it is how this process cascades down to suppliers’ suppliers, as though some kind of national emergency had been called.

In short, everyone takes a hit and reorganizes. Obviously, there is an end point to this (such as the spot prices of mineral commodities), but consumption rates, technical improvements in manufacturing and efficiency gains can go a long way to offsetting how much slack is still in the system before hitting rock bottom.

Impacts on the global sector in 2026 and beyond

When costs get reset across the silicon value-chain in China during the first half of 2026, the PV industry will be entering a new phase when annual terawatt production numbers become a routine occurrence.

Also, it will be the start of the final optimisation of the single-junction solar technology which is by default back-contact process flow architectures.

Getting costs under control during the second half of 2025 and the first half of 2026 is important for the leading Chinese PV companies as it will allow for capital spending: for upgrades from TOPCon cell capacity (and to a lesser extent, module assembly) to back-contact cells; and for any overseas investments that are deemed commercially attractive.

Should this all go as I expect, the impact will be felt mostly by PV manufacturers in all other countries/regions (that will have based cost models and business plans on metrics that are no longer valid) and by module buyers (with a blend of positives and negatives).

When looking at what the U.S. PV manufacturing sector is having to deal with today, it seems that the U.S. and China look set to diverge even more.

Manufacturing in the U.S. was precariously balanced even when Chinese costs were 2X today’s levels and the production incentives in the U.S. were deemed low risk (and before FEOC became a potential showstopper).

Fast-forward twelve months from now – with costs under control in China and U.S. manufacturing having (at best) treaded water from a weak starting point – and the gap between terawatt production reality (in China) and everyone else (not just the U.S.) is going to be a major wake-up call.

Perhaps this is a glimpse into what the solar PV industry will look like in the coming terawatt era. But for now, scrutinising that cost equation in China is the most important metric to track.