The most important issue for the solar photovoltaics (PV) manufacturing sector in 2025 is cost-reduction, not pricing-recovery.

This article reviews manufacturing costs (specific to the major vertically integrated global leaders in China) – and how these have trended to the end of 2024 – and considers how costs can be further reduced in 2025 to restore manufacturing profitability of the Chinese PV sector.

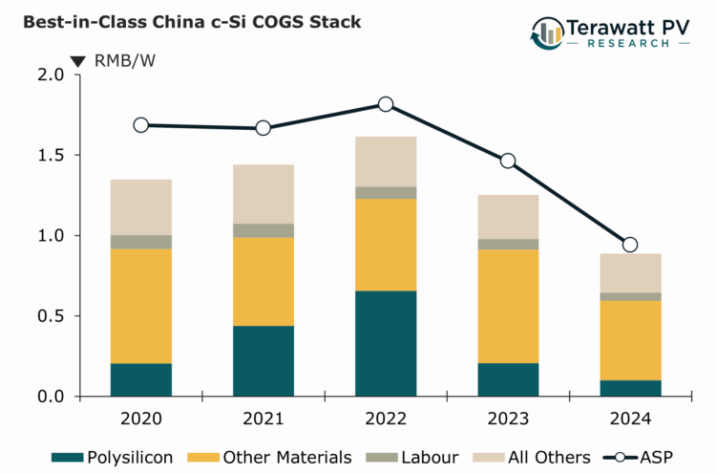

Entire China supply-chain working as single unit

The graph above shows the cost-of-goods-sold (COGS) stack over the five-year period 2020 to 2024, with the blended average selling price (ASP) of modules (upper line).

The data was extracted by auditing the accounts of the leading module suppliers over this period, in addition to these companies’ leading materials suppliers (also mostly, if not all, China-based).

While polysilicon price increases from 2020 to 2022 were largely offset by an end-market that was in under-supply and could cope with module ASP increases, the broad over-supply in 2023 and 2024 then forced the collapse of polysilicon pricing (which is likely to continue for the whole of 2025 and 2026).

By the end of 2024, the module COGS was at parity with module ASPs, resulting in heavy operating losses for the not just module suppliers, but the entire materials supply-chains.

2025 is the year of cost resetting, with nothing meaningful left to be squeezed from polysilicon. The focus today is to reduce costs of the other materials; crucibles, diamond wires, silver paste, encapsulants, glass and frames.

Except for silver paste supply, all other materials suppliers are having to work on costs, in a way that was not essential over the past 5 years. Losses from most suppliers in these categories have been reported for the past few quarters.

Essentially, there is a cascade of cost-reduction until reaching critical raw materials and commodity cost levels that are outside the control of the supply-chain.

By the time annual production at the terawatt level is reached, the PV industry will be living in a material world.

Tracking progress during 2025

Within a few weeks (once half year results are released), it will be clear how much progress is being made towards restoring gross margins at the 10-15% level (for the module suppliers at least).

Also, this will allow a better understanding of how much work is left to be done for some of the major wafer and cell suppliers (themselves benefiting from the cost-reduction done by the leading Chinese players), not to mention glass suppliers (now possibly the key segment to review).

Cost reduction is the dominant metric to track in the PV sector today, more so than technology-change, pricing-uptick speculation or rhetoric from China related to industry capacity rationalisation.

If costs can be put in order in China by the end of 2025, the ‘official’ end of the manufacturing downturn can probably be called, allowing 2026 to be the year of mass migration from TOPCon to back-contact.