Among the list of casualties of the second PV manufacturing downturn is a subset of Chinese heterojunction solar cell entrants, swept into the sector on the back of domestic-driven and over-ambitious technology roadmaps.

This article represents the first detailed analysis of a subset of public-listed Chinese heterojunction PV manufacturers that ramped up production lines during 2023 and 2024.

A host of metrics is examined for this group, including actual production volumes, heterojunction-specific capital expenditure (capex), profitability and debt.

China’s fascination with heterojunction a nod to Sanyo’s ground-breaking technology-leadership

While China established itself as a leader in PV manufacturing 15 years ago, the know-how and intellectual property relating to the premium technology offerings of the day were retained by SunPower (for back-contact cells) and Sanyo (for heterojunction).

As Sanyo exited the sector and certain patents owned by the company expired, companies in Taiwan and China took their first steps at moving into the heterojunction space.

Interestingly, this period (circa. ten years ago) overlapped with the demise of global efforts to commercialize amorphous silicon (a-Si) based thin-film PV, with significant investments in China (from the likes of Hanergy and Gold Stone) having been stimulated by government initiatives at the time aimed at onshoring expertise in certain strategic technologies.

While the move to ‘retrofit’ shuttered a-Si fabs (often including deposition equipment from Applied Materials, Oerlikon and ULVAC) to crystalline silicon (c-Si) heterojunction cell lines was not confined to Asia (notable players also being Hevel and 3Sun), it was clear that Chinese companies (including the major tool suppliers to the sector by then) were positioning themselves in an attempt to replicate Sanyo’s technology with a lower cost model.

Pivotal decision point in 2020 goes in favour of TOPCon

With the PV industry having made its transition from p-type multi to p-type mono PERC in 2020, the search was on for the ‘next’ technology upgrade within the sector.

Returning to the three main technology options of the time (n-PERT/TOPCon, heterojunction and back-contact) that could be chosen when moving from p-type to n-type, efforts began apace in China, focusing largely on TOPCon or heterojunction as the preferred candidates.

Most of the leading Chinese cell producers evaluated closely the pros and cons of TOPCon and heterojunction, with all the main players choosing TOPCon. The argumentation at the time was largely swayed by the seamless transition from PERC to TOPCon, tool availability in China and perceived lower capex.

In hindsight, the move from PERC to heterojunction could easily have been effected at the expense of TOPCon, with heterojunction having certain well-known and inherent advantages over TOPCon.

However, TOPCon was the chosen technology and has by now become the mainstream offering to the sector (in the same way that PERC was back in 2020).

This effectively created a niche subset of stakeholders championing heterojunction, with the technology being lauded by Chinese trade associations and research-based entities – something that still exists today, despite everything that has happened in the sector regarding technology in the past few years.

China heterojunction investments gain traction

Post 2020, investments into new heterojunction cell capacity gained traction, often pitched as being a ‘superior’ (or even somewhat spuriously as a ‘next-generation’) technology to TOPCon that was rapidly becoming the mainstream n-type offering to the sector.

Outside China, companies such as Meyer Burger, 3Sun (ENEL) and REC Solar (then owned by a subsidiary of a state-owned Chinese company, now by Reliance) doubled down on in-house efforts to create a non-Chinese, non-TOPCon product offering.

However, the real heterojunction action was in China at this time and included a diverse range of stakeholders.

State-owned entities set up research pilot lines and efforts. Existing c-Si cell/module suppliers (already fixed on TOPCon investments) created heterojunction pilot lines, largely as a defensive play. New companies entered the sector, either created specifically to focus on heterojunction cell (or cell and module) production, or through back-door listings via existing Chinese companies whose market proposition was in decline.

Heterojunction investment announcements from China were a common feature in the sector during 2021 to 2023, with over-enthusiastic observers often compiling lists of announcements that harked back to the days of the industry’s thin-film indulgence some 15 years ago.

As expected, many of the announcements failed to come to fruition. Others pivoted from dual heterojunction/TOPCon options to simply TOPCon capacity investments.

However, a subset of about a dozen in China made it to production line equipment build-out, with many of the new entrants starting as pure-play heterojunction cell producers and even having some early success in selling heterojunction cells to the likes of REC Solar in Singapore for REC’s overseas module shipments.

Over this period, Huasun had emerged as the clear heterojunction leader in China (and globally). Along with the only major established Chinese player in the sector at the time to invest heavily in heterojunction cells for mass production (Risen), these two companies started to account for utility-scale heterojunction module shipment volumes never seen in the industry before. (Sanyo and the likes of REC had focused on rooftop deployment).

Transparency on heterojunction metrics historically a black-box

Until recently, all previous industry activities making heterojunction cells had been undertaken by divisions (or sub-divisions) or business units of very large entities (such as Sanyo/Panasonic), with key manufacturing metrics (production, yield, capex, margins, profits, return-on-investment) not discussed or revealed by the companies.

One was left simply to surmise that such operations were loss-making and lost in the noise during financial reporting; investments largely written off in a blue-sky R&D manner.

And with Huasun being a privately held entity (also not having gone down the IPO draft filing route) and Risen’s heterojunction activities consolidated fully in the company’s multi-technology and business-unit organizational structure, any immediate visibility into the heterojunction specifics of these two market leaders in China has been challenging at best.

Indeed, until recently, visibility into the commercial operations of heterojunction technology had been one of the PV industry’s most gaping holes – in contrast to the transparency of operations for all other PV technologies over the past 30 years.

Chinese listing obsession to the rescue

In early 2024, most of the active Chinese players in the heterojunction ‘space’ got together, seeking to promote the technology as a single voice, under the title of the ‘740W+ Club’, subsequently upgraded 12 months later to ‘760W+ Club’.

While by far not a full list of all PV companies in China that had invested in heterojunction cell lines since 2020, it did include the participation of the two leaders (Huasun and Risen), many of the large entities (such as Shanghai Electric, CNBM and SPIC) that had set up R&D activities (possibly simply as skunkworks operations), and a group of new PV market entrants (four to be specific) that were seeking to become pure-play heterojunction public-listed PV companies.

Therefore, with the inclusion of one other China frontrunner in heterojunction cell investments (Akcome), this provided a list of five companies to dissect in detail – for the first time .

Before looking at the findings in more detail, it is worth noting that the listing obsession in China in the past few years (or simply from share placements and H-Share filings) has also allowed heterojunction metrics to be understood in greater detail, such as from several silver paste and powder suppliers. This helps considerably when understanding the overall heterojunction landscape today, including the materials purchases from some of the privately-held entities operating somewhat in stealth mode.

Heterojunction mountain of debt revealed

To get a feeling for the scale of the subset of the five public-listed Chinese heterojunction producers analysed in this blog (referred hereafter as the ‘Group’), some of the key metrics are summarized first.

Between 2020 and 2023, this Group announced plans to build 52 GW of new heterojunction cell lines by 2026, across 12 different sites in China (mostly with the expectation of regional investments or joint facility ownership).

Recall that lists of ‘announcements’ of this type in the media comfortably exceeded 100 GW in China during this period. However, already the relevance of the Group should be clear, given that the five companies were among the dozen or so that ended up building new factories and equipping them with heterojunction lines.

By the end of 2024, approximately 8 GW of heterojunction cell lines had been installed and commissioned from the Group of companies, almost all turn-key lines from different Chinese equipment suppliers.

Again, to put this in context. When one excludes the heterojunction cell capacity installed by Huasun and Risen (and all the pilot lines that are not contributing to industry effective capacity levels), this figure of 8 GW likely accounts for more than 75% of the ‘real’ heterojunction cell capacity that exists in China today. As such, how these five companies in the Group have performed when operating the new heterojunction capacity should be highly relevant.

The new analysis outlined in this blog is performed by consolidating a host of company-specific heterojunction metrics (across ramped capacity, production, yield, average sales prices, cost of goods sold, capex, assets, liabilities, profits, etc.) into overall Group numbers and then treating the performance of the Group as a single heterojunction ‘entity’. In reality, the companies show very similar trends with no outliers skewing this approach.

The goal of this analysis was to see how the heterojunction specific investments had changed the performance of the Group as a whole, noting that most of the companies had been clinging to the hope that the move into heterojunction cell production would have positive outcomes.

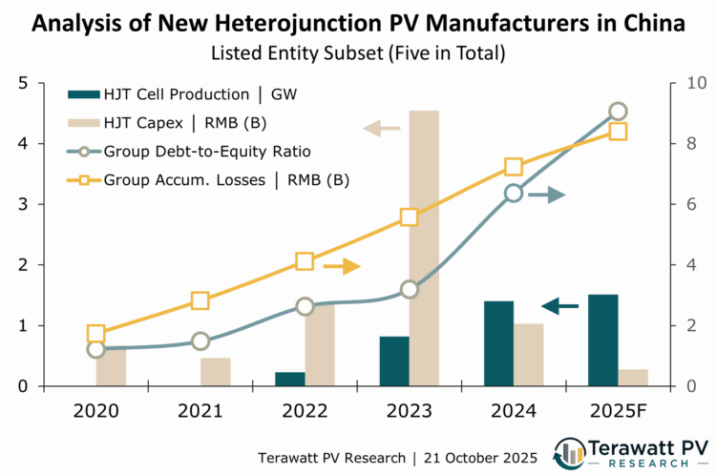

Four key metrics emerged from the analysis and are shown on the same graph for clarity (Figure 1 above). The findings are now discussed and explained.

The light-brown vertical bars capture the level of investment (heterojunction-specific capex), plotted on the primary vertical axis (left side) in RMB (Billions). This shows a clear spike in 2023 at 4.53B RMB (circa. US$650M), as the ‘initial’ batch of the ‘planned’ 52 GW was installed. Over the 3-year period 2022 to 2024, heterojunction capex from the Group was just under US$1B.

The collapse in the heterojunction capex (2024 and 2025) of the Group is best understood once the other (inter-related) metrics are covered.

The net impact of this US$1B capex was about 8 GW of operational heterojunction cell capacity installed by the end of 2024. While this may seem ‘small’ when considering the >50 GW plan, one should remember that grand plans should be taken with a pinch of salt at the best of times. And that 8 GW of heterojunction cell capacity in China (once Huasun, Risen and all the pilot/R&D lines are excluded) is quite an achievement.

However, the usefulness of this circa. 8 GW of heterojunction cell capacity is another issue. Now look at the second vertical bar (dark blue) which plots annual heterojunction cell production levels from the Group (primary left vertical axis, in GWp-dc).

Heterojunction cell production was below the 1-GW-level in 2023, reached about 1.5 GW in 2024 and is trending somewhat flat so far in 2025. Immediately, it should be clear that a yield figure (production as a percentage of ‘available’ installed and effective capacity) at the 20% mark is not a good sign, and probably indicative of other issues impacting a business in general.

To examine the impact of the heterojunction capex and manufacturing on company operations, two Group-level metrics are shown on the graph above; the debt-to-equity ratio and the accumulated losses (noting that any accumulated profits for this Group predates 2020).

The accumulated losses (yellow line, secondary right vertical axis, in Billions of RMB), show a near-linear year-on-year increase through the investment and operational phases of the heterojunction sites.

As the focus on heterojunction as a major ongoing strategy took grip during 2021-2022 (at the expenses of other revenue streams or accompanied by the disposal of non-core assets), accumulated losses simply kept increasing. By the time the bulk of the heterojunction capex had been committed (2023), the level of accumulated losses was exceeding the asset value of the heterojunction Group, effectively flipping the Group into a state of negative equity.

As heterojunction manufacturing was ramped up (2023-2024), immediate operating losses were incurred at excessive levels. Some of the heterojunction cell makers in question were reporting negative gross margins in the range 20-40%, almost in fire sale mode from the off.

Consequently, accumulated losses have continued to grow, with the Group total close to 8.5B RMB, versus an asset value of less than 2B RMB and a trending annual turnover of just 2B RMB.

Somewhat unsurprising then should be the trends seen when looking at the Group debt-to-equity ratio (light blue line, secondary vertical axis). Starting again at precariously high values, between 1.5 and 2, this ratio has grown to near-fatal levels close to double-digit territory.

In short, the very investments (heterojunction manufacturing) that were intended to restore the fortunes of these hitherto stagnant or slowly declining entities had the unintentional consequence of plummeting ongoing operations into a state of near paralysis.

While no individual operating metric outside its comfort zone is a cause for alarm, quarter-by-quarter declines in cash-flow, debt and profitability represent a cocktail of calamity, especially in the absence of any other profitable revenue streams or plan to reverse the operational problems in the first place.

Inevitably, the outcome is a combination of delisting notices, freezing of assets or enforced change of ownership to a China state-owned distressed-asset fund, ahead of finding a new private entity ownership structure in the future.

Heterojunction 3.0 largely in Huasun’s hands

While the failure of the heterojunction Group discussed above is particularly concerning, there is no shortage of new cell production entrants in China in recent years that chose TOPCon as the technology of choice and were confronted with an oversupply environment that resulted in heavy loss making. However, the magnitude of the losses for the TOPCon entrants has not necessarily driven these companies to imminent insolvency.

In part, the lack of viable heterojunction cell producers in China now puts more pressure on the main proponent of the technology, Huasun, to champion the technology through its next generation offering. In its favour, Huasun has established an economy-of-scale not seen before for heterojunction but is now at risk of being a niche-technology player in a mainstream focused on moving TOPCon to its next iteration or indeed moving directly to full back-contract variants. The analogies here to First Solar being the sole player in the thin-film space today are self-evident.

Rather, it could be that increased scrutiny is now needed on the scattering of the heterojunction projects underway (or being proposed) in the U.S. and India, with the rationale for certain companies to align with heterojunction cell builds in the U.S. being driven by non-technical factors (IP and patent related to TOPCon processing).

Regardless of how technology pans out in the coming years, China’s investments in heterojunction have already been pivotal in advancing certain aspects of c-Si wafer and cell production that may not have been prioritized so early in full TOPCon efficiency and cost optimization (increased copper content in metallization and the use of thinner wafers, to name just two).

Ultimately, as the sector fully optimizes ‘single’ junction c-Si cell architectures, learnings from all three n-type architectures (TOPCon, heterojunction and existing back-contact designs) will feed into the next iterations of cell design out to 2030.

Perhaps, after all, technology competition can only be a good thing for the sector as a whole, so long as you can remain competitive during any shake-out and fully benefit from the accumulation of learning that was undertaken at the time.