Solar photovoltaic (PV) equipment suppliers in China are set to be among the most severely impacted by the ‘second PV manufacturing downturn’ of 2024-2026.

Chinese PV equipment suppliers had only recently been riding a wave of optimism between 2020 and 2023, as their domestic customer base released a succession of purchase orders to fuel capacity expansions in mainland China and across Southeast Asia.

However, manufacturing downturns are caused by cyclical capital expenditure (capex) dynamics. Therefore, it is inevitable that equipment suppliers will be heavily impacted – and likely more than their customers (PV ingot-to-module manufacturers), or indeed PV materials suppliers that serve production needs (not capacity).

The downturn of 2024-2026 is not the first time the PV industry has been subjected to a manufacturing downturn, but what distinguishes this event from the previous downturn (between 2012 and 2014) is the scale of the problem, and the magnitude of the ensuing headcount reductions on the production floors across China.

This blog explains why PV equipment suppliers in China have essentially been caught up in a PV manufacturing eco-system in China that had been collectively focused on capacity expansion as the only game in town, with little thought given to external factors that could derail this obsession.

The story starts more than 20 years ago

When the PV industry moved from research to mass production, fabs were equipped with tools from suppliers that had been aligned to the research communities of the day and the early movers in manufacturing across Japan, the U.S. and Europe.

At this time, tool suppliers included the likes of Centrotherm, Schmid, Rena, Roth & Rau, Meyer Burger, GT Solar, Despatch, Baccini, Komatsu, and Sumitomo. Consequently, PV equipment from these suppliers was heavily utilized during the first wave of c-Si capacity additions throughout the wider Asia region (Taiwan, South Korea and China).

While the prospects for c-Si manufacturing in Taiwan and South Korea largely dissipated before gaining traction, China created a domestic eco-system of equipment and materials suppliers that ultimately led to the demise of almost all Western PV equipment supply business models.

This newly created Chinese domestic c-Si PV eco-system then coalesced perfectly to support the growth of the PV industry from tens of gigawatts annually to current levels of more than 600 GW.

Until the first half of 2023, nothing looked amiss with this China PV model, where investments in new capacity were purposefully channelled into the country’s domestic equipment and materials suppliers.

However, the foundations of this eco-system were based almost entirely on strong and sustained annual growth rates for the PV industry, and a presumption that China would continue to dominate equipment, materials and component manufacturing (producing in mainland China or across Southeast Asia to avoid trade barriers).

The modus operandi also assumed a degree of co-operation between the leading stakeholders, allowing companies to report modest shareholder returns, despite the downward pricing trajectory of products being sold.

Fast forward to the end of 2024 and the Chinese PV manufacturing sector was in disarray. The second PV manufacturing downturn had taken grip and China’s PV equipment suppliers were likely going to be the most severely impacted.

Let’s look briefly now at why this change in events occurred.

Incumbent complacency & new-entrant fantasy

At the start of 2022, signs were emerging that a deluge of new purchase orders for Chinese PV equipment suppliers was about to unfold.

Existing c-Si component suppliers that had been GW-scale producers were planning to move to 10 GW levels. The current 10-GW pack was costing out capacity expansions to the 20-30 GW level. And market leaders were building fabs to increase capacities well above 50 GW and, in some cases, exceeding 100 GW at certain stages in the value-chain.

Now add to this a new influx of entities in China from non-technical backgrounds that seemed to think becoming a pure-play solar PV wafer or cell producer would transform their once stable and moderately profitable companies into scalable and lucrative entities that would be championed routinely in global Fortune 500 listings.

Maybe one or two speculative plays here would not have been newsworthy; lost in the noise when set against the broad countrywide capacity expansion fervour from the incumbents.

However, during 2022 and 2023, more than 50 companies in China decided to embark on this journey of delusional fantasy, entering an already overcrowded sector with no product differentiation, no existing technical or market knowledge, and no strategy to deal with any changes in market conditions by the time they had ramped up new production lines.

The net effect of the aggressive expansion plans from existing manufacturers and investments from the new entrants was a capex bonanza in China during 2022 and 2023. Consequently, the order books of Chinese PV equipment suppliers ballooned to record levels.

Everything looked to be fine for a while. Equipment companies in China added production headcount to meet this upsurge in bookings. Deliveries were in full flow.

However, capacity additions through the entire value-chain were grossly out of proportion and would have required end-market demand to show instant elasticity (effectively consuming anything produced on tap) in a way that was completely unrealistic.

The Chinese PV eco-system was essentially on a one-way track to destruction. Even if 2024 had worked out in their favour (with the end-market globally snapping up cheap modules literally as they came off production lines), the investment vigour would only have been replicated year-after-year until the inevitable self-implosion.

And while production volumes and module shipments during 2023 and 2024 were at record levels, pricing everywhere (through the value-chain and down to materials suppliers) simply collapsed to the point that working-capital and debt replaced shareholder-return and capex as the key metrics to understand in China.

By the start of 2024, the salient features that are characteristic of a manufacturing downturn began to unfold. The past 18 months has seen PV manufacturers terminate new capacity plans (aside from some minor tactical overseas arrangements to access the U.S. market), sell off non-essential assets and accept that cost-reduction (not a meaningful price recovery) needs to be addressed going forward. Indeed, ‘gross margin recovery’ has become the PV manufacturing phrase of 2025 and will continue this way through 2026.

However, when looking across the Chinese PV eco-system today, there is one parameter that appears to be out of synch.

Why do China PV equipment supply results look so healthy during 2024 & 1H’25?

Manufacturing downturns shake out sectors like nothing else; in particular, for the very companies that live off capex – namely, equipment suppliers.

Indeed, during the first PV manufacturing downturn of 2012-2014, the impact was seen directly through the immediate declines in PV-specific new order intake at the leading PV equipment suppliers of the time (most notably then at Meyer Burger, Centrotherm, Baccini and GT Solar – although the ability of Asia to reverse engineer by then had started to eat into these companies’ market shares).

A classic book-to-bill for the PV equipment sector – such as those I used to do routinely 15 years ago as a market analyst at Solarbuzz – effectively illustrates the key metrics to study through a manufacturing downturn and recovery; the interplay between (net) bookings (new order intake less de-bookings), recognized revenues (‘rev- rec’) from shipments, and (credible) order backlogs.

During a downturn, one would expect the correlation between capex (customer driven spend) and equipment revenues (supplier payments) to be closely related. Certainly, this is (or should be) the case when customers and suppliers are adhering to similar accounting practices in reporting.

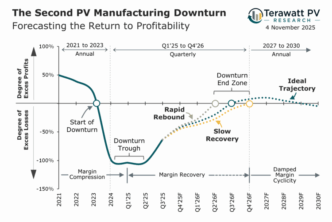

Consider now the second PV manufacturing downturn, starting in 2024. PV capex (best confined to c-Si ingot/wafer and cell/module stages from a phasing standpoint) indeed fell off a cliff in 2024, with 2025 even lower as expected – this coming from the market-leaders putting the brakes on major capacity expansions and the demise of the new entrants discussed earlier.

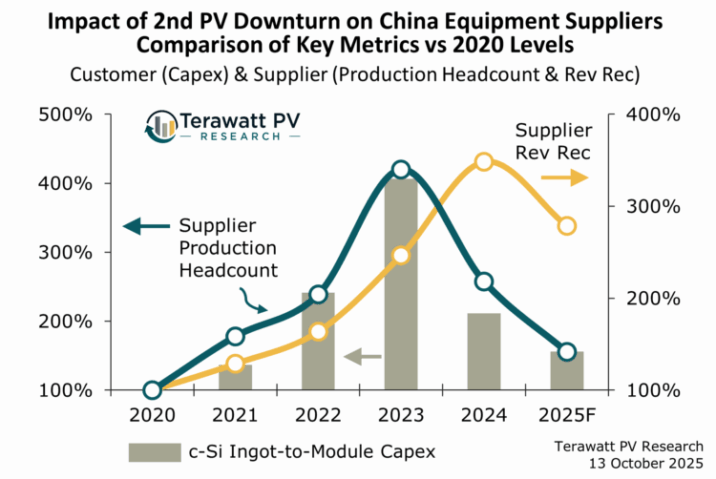

To illustrate the anomaly in 2024 China PV equipment supplier turnover, consider the graph shown above (Figure 1) to accompany this post.

The vertical bars (columns) in the graph show the trends in PV capex (specific to c-Si ingot/wafer and cell/module stages). The vertical scale is based on the percentage change per year, anchored to 2020 as the reference point. For example, in 2023, the PV capex figure of 400% basically means that PV capex in 2023 was 4X the level seen in 2020.

In reviewing the annual changes in the PV capex bars in the graph, it shows again why capex is one of the most valuable leading indicators to track as an analyst in a sector that is heavy on manufacturing spend.

To check out the correlation this time between PV capex and equipment supplier rev-rec, the operations of about a dozen of the leading PV equipment suppliers in China were analysed, focusing on companies where PV-specific bookings and revenues constitute a minimum of 80% of the company’s operations. In short, the main PV suppliers of recent that are effectively pure-play PV equipment entities.

This filtering is key to understanding the PV equipment landscape in China: otherwise, company metrics would be skewed towards other (non-PV) market segments, independent of PV-specific performance being split out (from a business unit segmentation perspective).

It turns out that the sample group of PV equipment suppliers analysed accounts for about 50% of all ingot-to-module PV capex in the sector during the five-year period from 2020 to 2024.

Therefore, trends extracted from this set of companies are almost certainly going to be replicated in the PV equipment suppliers excluded from the study (public-listed entities where PV equipment revenues make up a small proportion of company operations, and all private entities that are by nature not sharing this level of detail with the outside world).

The recognized (PV ingot-to-module specific) revenues for the PV equipment supplier sample group by year was then compared (like PV capex outlined above) to 2020 baseline levels. The results are shown in the orange line in the graph above (plotted on the secondary axis).

Now, let’s return to the question asked in the sub-heading above: Why did China PV equipment supply results look so healthy during 2024?

This question also jumps out in the graph above by the dephasing in PV capex (brown columns) compared to equipment supplier revenues (orange line).

The answer to this question is due simply to the time lag in payments from customers (PV component manufacturers) to suppliers (PV equipment producers), and a business climate where it can be up to two years from tool shipment before final payments are made/recognised (if indeed, they are even completed). Different payment terms exist in practice, but the net effect is that revenues (recognized and reported) lag audited capex commitments by, on average, circa. 12 months.

This explains why 2024 looked like a bumper year for Chinese PV equipment suppliers, reporting record revenues at precisely the same time as their customers had slashed capex budgets.

This prompted a search for other metrics that could be correlated in real time to PV capex; in particular, as leading indicators to forecast future revenue returns for the PV equipment supply-base, and to understand when revenues would start to reflect properly the downturn in spending.

Production headcount the ultimate backlog metric for PV equipment suppliers in China

New-order-intake and bookings-backlog are seldom spoken about in Chinese company reporting. In the rare cases that backlogs are revealed (often only in IPO prospectus filings to suggest future earnings potential), they can largely be taken with a pinch of salt, given the fragility of signed contracts from often debt-laden customers.

Even accounts-receivables volumes can largely be ignored, as often these are heavily populated by bad-debt provisions from zombie or insolvent customers, ultimately being unrecoverable and written off at some point in the future.

In the end, it turned out that one of most basic metrics used to assess manufacturing entities – production worker headcount – provided the best route to relate PV capex to the levels and phasing of future revenues from Chinese PV equipment suppliers.

Elsewhere globally, other business models exist where this type of analysis would not be valid; for example, in sectors where companies operate ‘fab-lite’ or ‘fabless’, or where manufacturers outsource the bulk of their production to OEMs or sub-contractors.

But this is not how the PV industry operates from an equipment supply standpoint. Production headcount numbers turn out to be an excellent input to any forecasting model.

Production headcounts were extracted for the near pure-play Chinese PV equipment supplier grouping analysed, by backing out contributions from sales, marketing, administrative, R&D and after-sales/service employee counts.

Changes in production headcount were then reference to 2020 levels and are shown in the graph above by the dark-blue line. The correlation between customer-driven PV capex and supplier production headcount is excellent.

Therefore, current headcount numbers can be used to generate a ‘real’ order backlog figure at any given time, and by default this allows new order intake (or bookings) to be calculated.

In short, it allows a book-to-bill ratio to be done at the company level for certain leading PV equipment suppliers in China and I will return to this in coming months when looking for signs that the downturn is coming to an end.

Until then, consider my initial workings here, shown in Figure 2 below, comparing book-to-bill trends for the two manufacturing downturns so far in the PV industry.

What does this all mean for China’s PV equipment suppliers?

This question has several answers.

First, it forecasts that 2026 will see strong declines in revenues for most PV equipment suppliers whose business models are heavily dependent on the PV industry. On a more granular basis, the major downturn may become apparent during Q3’25 or FY’25 reporting and simply continue at low levels of reported revenues all through 2026.

It also reveals the scale of the production headcount declines in China. Using the analysed grouping as representative of the whole PV equipment sector in China, I estimate that more than 35,000 has been lost in production headcount over the past 18 months – about two-thirds of the levels seen at the peak of equipment production at the end of 2023. China’s PV equipment supplier headcount figures by the end of 2026 could even return to levels seen back in 2020.

The forecast out to 2027 also suggests that many of the PV equipment suppliers in China will have to rely on maintenance-only capex from their customers or any upgrade spending at the tool level. This is particularly true for Chinese PV equipment suppliers whose business was largely making one product for one customer (such as an ingot puller for new production lines set up by LONGi).

However, some of the PV equipment suppliers in China have been actively seeking to find new business outside China; in particular, from the U.S. and India (not to forget Chinese investments in the MEA region). While the volumes here will never come anywhere close to the Chinese deluge of 2022-2023, the opportunities arising from India and the U.S. are coming at the right time. Although, in 2024, the revenues from the leading PV equipment suppliers in China were still heavily weighted (typically 80-90%) to domestic sales.

While order intake swings of the order seen in the past few years would likely sound the death knell for any Western equipment supplier, dependent on the PV industry, the leading Chinese PV equipment suppliers will likely reset going forward. Years of operating asset-lite and selling tools with gross margins in the range 25-30% – while operating now with significantly lower labour costs – will prevent any major red flags from an ongoing operations perspective.

However, the big question here relates to where the next major uptick in new order intake will come from.

Normally, manufacturing downturns are characterized by the emergence of new technology-spend phases that will gain market-share when the downturn is finished. However, this is far from clear in the PV sector today and will be discussed in more detail in a separate blog post shortly.

The pause in PV equipment spending is now focusing the attention of the Chinese equipment suppliers on adjacent technology segments, in particular seeking to increase semiconductor revenues. This had been a goal for years but was likely sidelined owing to the immediate business opportunities that were presented by PV customers. Therefore, this will be a space to monitor closely going forward.

It will be a further six months before the full impact on the Chinese PV equipment supply chain arising from the PV manufacturing downturn is known. Strategies will likely be reset once 2025 is completed and the preamble in 2025 annual reports released in April 2026 will be eagerly dissected. By this time also, the opportunities for new c-Si capacity additions in the U.S., India and elsewhere will be clearer to see.

And who knows? 2027 and 2028 could be worth the wait if a terawatt of TOPCon capacity in China needs to be retrofitted for the next-big-thing!